AMAT. No Beat, No Raise, No Slump. But Why?

AMAT. No Beat, No Raise, No Slump. But Why?

WFE valuations are at all time record highs while revenues remain on life support from China

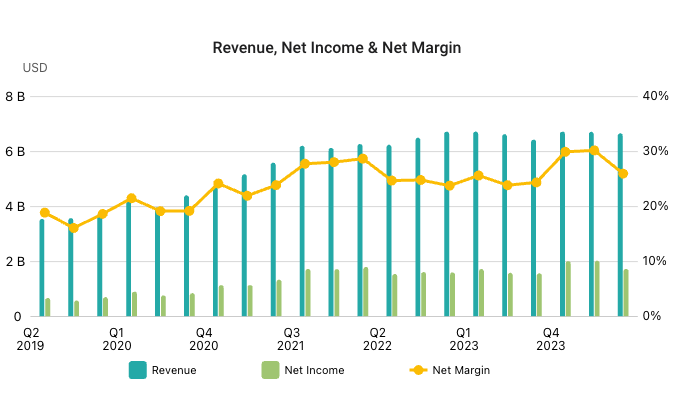

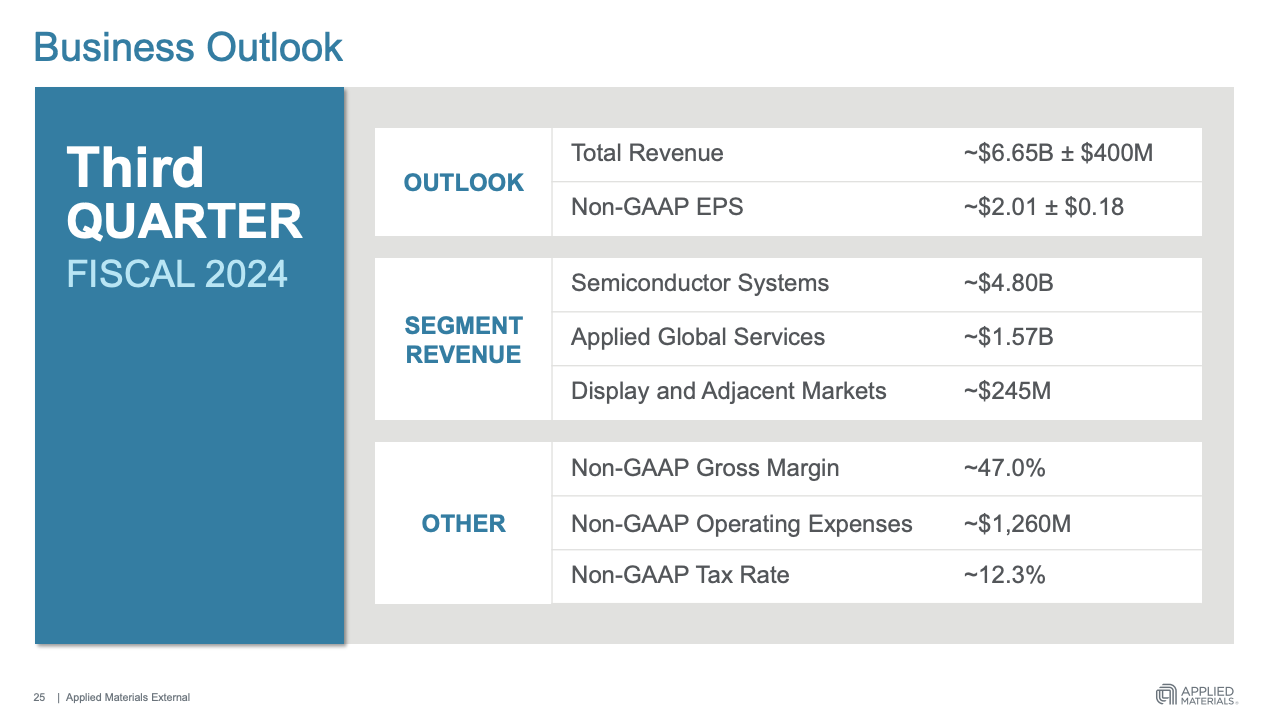

AMAT last week announced revenues for their latest quarter of $6.65 billion, in line with guidance and essentially flat both QoQ and YoY.

Looking ahead, the company forecasted more of same with current quarter revenues of $6.65 billion at the midpoint and gross margin stable at 47%

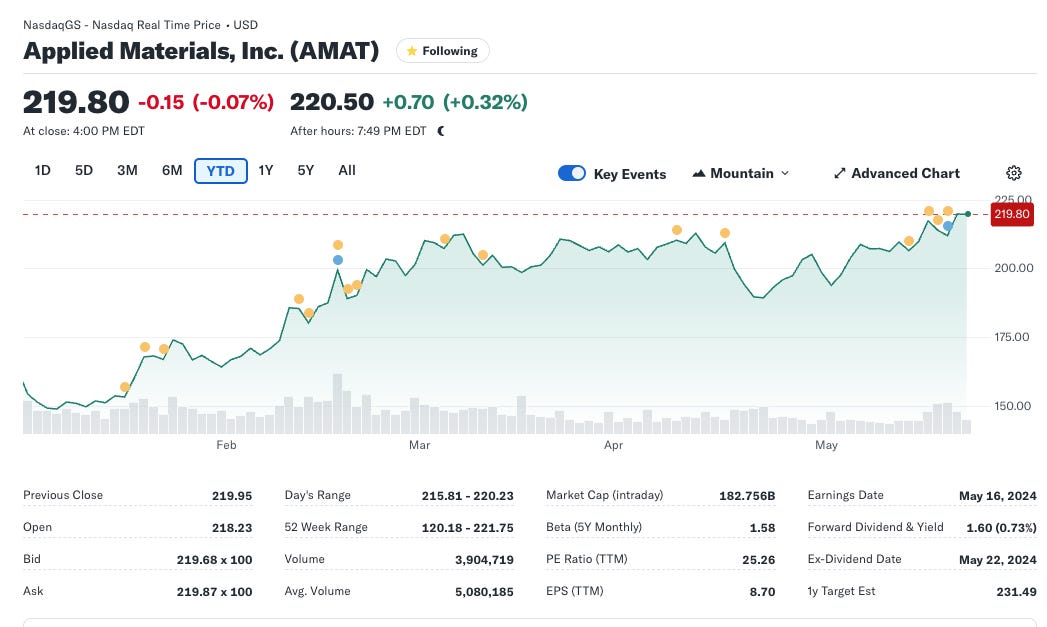

Under these no beat, no raise circumstances, one might have anticipated a meaningful slump in the share price, but this was not the case. While there was indeed a slight downward movement post earnings, AMAT has since gone on to reach an all time record high of $221. It sits today just a shade under that price at $219.8

It should be pointed out that AMAT is not unique here. All of the leading WFE players are at or close to all time record highs. Indeed, LRCX’s recent announcement of a $10 billion share buyback along with a 10 for 1 stock split saw their share price soar > 6% over the following two days:

"The share repurchase authorization announced today will execute over an indeterminate period of time and is consistent with our plan to return 75% to 100% of free cash flow to stockholders in the form of dividends and share buybacks," said Doug Bettinger, Lam's Executive Vice President, and Chief Financial Officer. "Furthermore, the stock split announced today will enable a larger proportion of Lam's worldwide employee base to participate in the company's employee stock plans."

The markets clearly shrugged off AMAT’s no beat/no raise earnings report and are demonstrating unbridled enthusiasm for the key players in the broader WFE segment. Is this justified? Here’s our thoughts on the matter:

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.