ASML. Maintaining Guidance Despite New Bookings Sharp Decline

ASML. Maintaining Guidance Despite New Bookings Sharp Decline

New bookings fell precipitously in the first quarter

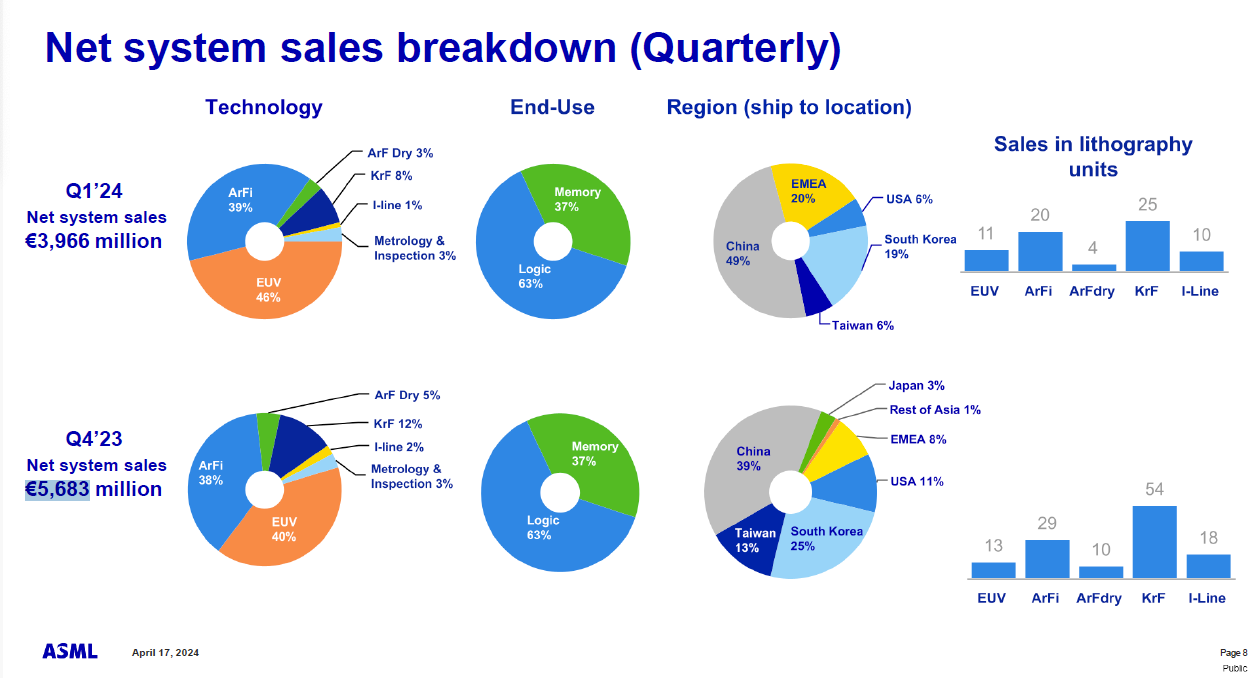

ASML reported Q124 revenues of €5.3 billion, in line with expectations, down 27% QoQ and down 21% YoY. Gross margin of 51% was marginally higher than forecasted. Net system sales were €3.9 billion, down from €5.7 billion in the prior quarter.

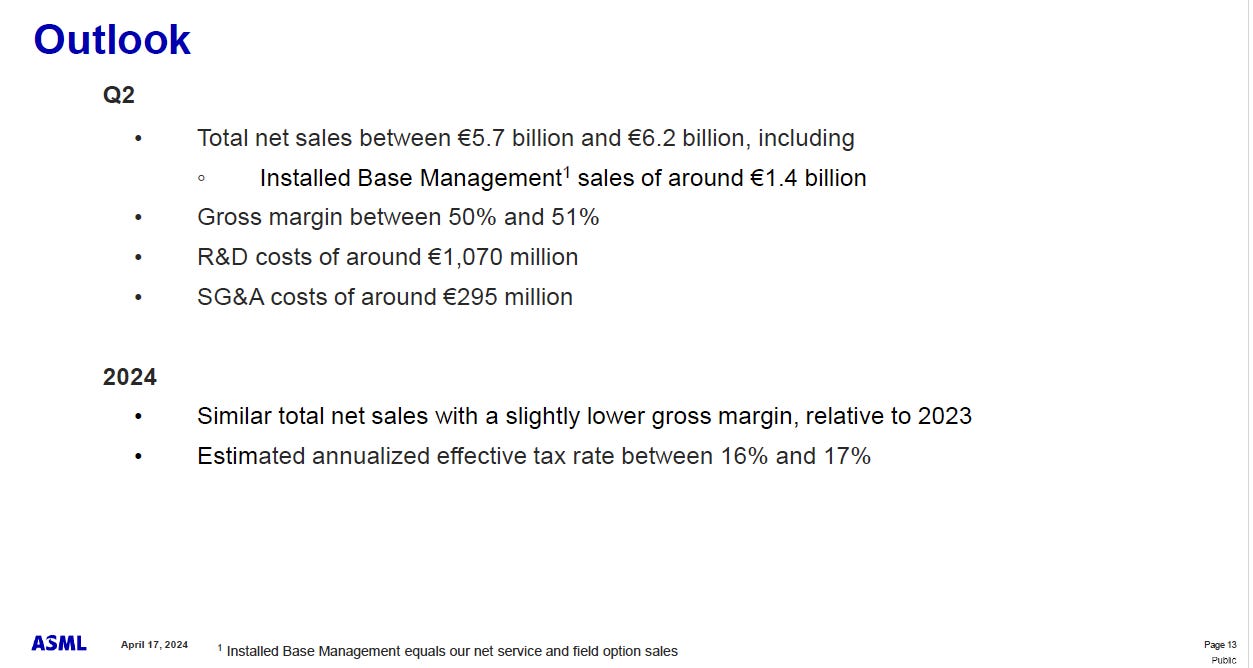

Net sales for the quarter came in at €5.3 billion, included in there €1.3 billion for Installed Base business. That €5.3 billion was smack in the middle of the guidance that we provided last quarter. As to gross margin, that came in at 51%. Better than what we guided. A couple of reasons. First there were some mixed effects. There was a bit more immersion and EUV in there in comparison to the dry business. There were also some one-off effects in there that drove up the gross margin to 51%.

The end-use split remained unchanged QoQ with Memory accounting for 37% and Logic 63%. In percentage terms, shipments to China jumped to 49%, up from 39% in the prior quarter. However, in absolute dollar terms , China shipments actually declined by ~€250 million.

In terms of outlook, ASML expects total net sales in the current quarter of €5.95 billion at the midpoint. For full year 2024, the company reiterated the guidance they have been providing for around the past six months at this stage, i.e. revenues to be flat sequentially with 2023.

Our outlook for the full year is unchanged with similar revenue compared to 2023.

The problem with ASML’s second quarter guidance is that it’s coming in around 23% down YoY. This means that for H124, ASML will be down >20% YoY. In other words, H224 is going to have to come in significantly higher than H124 in order to maintain the full year 2024 revenue goal of being flat to 2023.

The relatively low first half of the year, compared to the expected strong second half, is in line with the expected industry recovery from the downturn.

In line with the industry’s continued recovery from the downturn, we expect a stronger second half relative to the first half of the year.

To make matters worse, order intake in the first quarter dropped to €3.6 billion, down significantly from the €9.2 billion in the prior quarter. The combination of disappointing second quarter guidance and significantly lower order intake spooked investors and sent the share price down 7% in overnight trading. This latest downward move sees the company’s share price 14% below its 52 week high, albeit it’s still up very nicely from the $700 level it was at back in mid-January.

Below the fold, we discuss:

# ASML’s order intake during the first quarter

# expectations for their China market in 2024

# whether the latest price action is justified

# the significance of ASML’s first customer shipment of their next generation low-NA EUV tool, the NXE:3800E.

# their commentary on the overall semiconductor recovery cycle

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.