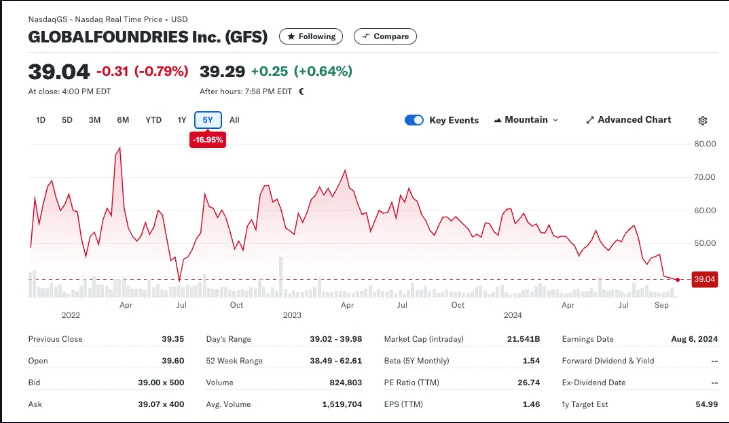

GlobalFoundries. Share Price Down 17% Below IPO Price & Down 30% Since July. But Why?

GlobalFoundries. Share Price Down 17% Below IPO Price & Down 30% Since July. But Why?

TSMC is on track for record growth while their second tier competitors are struggling..

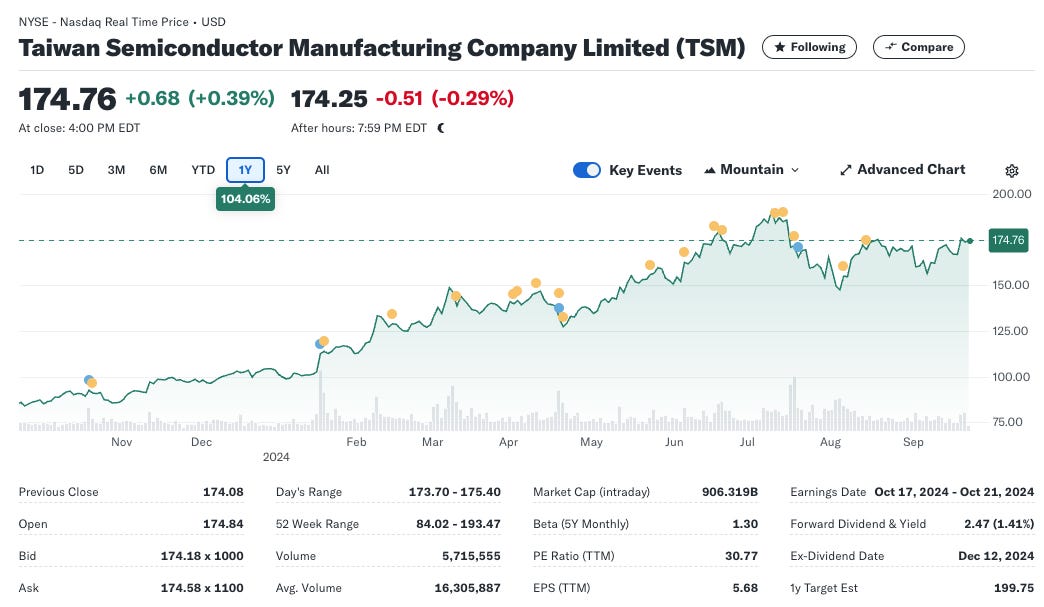

For some contrast first, let’s take a quick look at the global #1 foundry, TSMC. The company is on track to grow revenues by around 30% YoY in 2024. This growth is being driven primarily by strength in their HPC segment. More specifically, TSMC is benefitting handsomely from the soaring demand for AI acceleration chips. This has been reflected in the company’s share price which is up 104% over the past year.

TSMC’s share price did experience a decline from its all time high of $193 over the summer months and we wrote about the opportunity that presented in this note published on July 21:

The share price has since recovered nicely, presently sitting at ~$178. There’s another tailwind that recently arrived on the scene for TSMC. It came with little fanfare and received little to no media coverage. We covered it in this piece we wrote about Intel in early September:

You see, Intel cancelling their 20A process means that their entire production (apart from final packaging) of their next generation client processors, dubbed Arrow Lake, will now be manufactured by TSMC. First Meteor Lake, then Lunar Lake, now Arrow Lake. Of course there’s also the PC client processors TSMC makes for AMD, and the Snapdragon Elite X processors for Qualcomm. This is all purely in the PC client processor space. Long TSMC!!

GlobalFoundries

Globalfoundries share price has performed abysmally in 2024. It’s down ~30% since mid July. Even worse, it’s currently 17% lower than its IPO price almost three years ago.

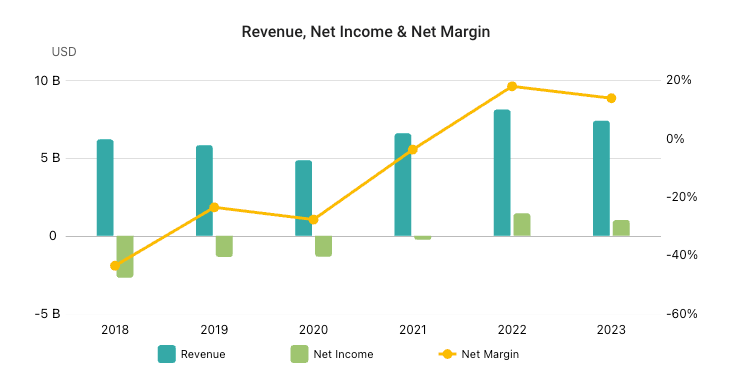

Yet, the company’s financial performance over this time period has been pretty good. When CEO Thomas Caulfield took over in early 2018, the company’s finances were a mess. Under his leadership, they’ve being better ever since. GFS turned net income positive in 2022, remained there in 2023 and set to continue to remain so in 2024.

In terms of FCF, GFS has generated over $500 million in H124 and is on track to triple their 2023 free cash flow for 2024 as a whole

Yeah we also had some benefit of the first half of some of our customer prepayments and accelerated AR collections that benefited first half free cash flow so, all things considered, good performance you know we generated more than 500 million dollars a free cash flow in the first half and are on track to meet our our goal for 3x improvement. That's actually up if you recall the prior indication was two and a half to three. We have upgraded that to three times 2023 free cash flow performance so we're pleased to report that this morning.

So what’s going on? GFS is being well run, is on a sound financial footing, is gradually exiting from the current downturn and generally has a bright future. Why does its share price keep falling? Let’s dig in….

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.