Globalwafers Q4 2022 Earnings Key Takeaways

Globalwafers Q4 2022 Earnings Key Takeaways

Bucking the trend with a sequentially flat CY2023 revenue forecast

Globalwafers held their Q4 2022 earnings call on March 14. As usual, it was a call replete with frank and interesting commentary on the company and the broader semiconductor environment.

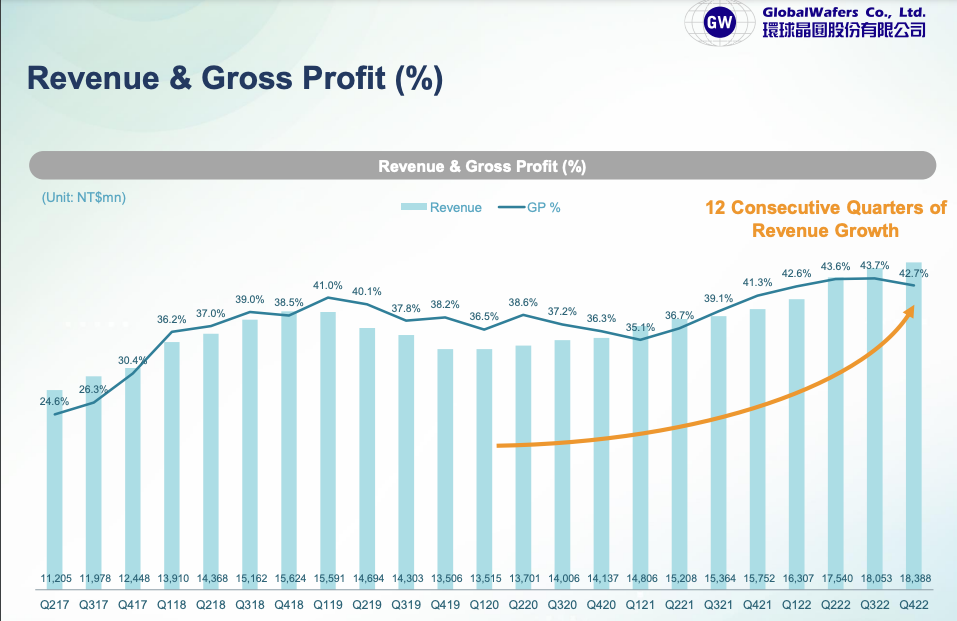

Q4 2022 represented the company’s twelfth successive quarter of sequential revenue growth, a remarkable achievement. Not surprisingly, FY 2022 was also a particularly strong growth year for the company:

Our growth momentum has been lasting for three years, starting from Q1 2020, which is consecutive growth for 12 quarters. 2022 again is our best ever year for GlobalWafers. First, our revenue hit a historical high with double-digit Y-o-Y growth. Our Q4 revenue totaled TWD18.4 billion with 16.7% Y-o-Y. Full year revenue in 2022 achieved TWD70.3 billion. This is a 15% increase Y-o-Y.

Gross & net margins also reached record levels in both Q4 and CY 2022:

Regarding to GlobalWafers' gross profit, our gross margin -- gross profit margin Q4 2022 hit 42.7%. In the whole 2022, full year gross margin hit 43.2%. This is a record high for us as well. And our operating profit margin in 2022 amounted to 35.5%. This is, again, an all-time high. We achieved the best quarterly net profit margin at 31.5% in Q4 2022. So in general, our overall revenue, gross margin, operating income and net profit are doing pretty well.

There was one fly in the ointment however, namely earnings per share:

And our EPS has been deeply correlated to the mark-to-market valuation of Siltronic shares, which has eroded our profits in previous quarters, owing to Siltronic's low share price, even though GlobalWafers managed to contribute the best effort in both quarterly and annual EPS, which were TWD13.31 per share in Q4 of TWD13.31 per share. And TWD35.31 EPS, earnings per share, this is our 2022 full-year's EPS.

Excluding the valuation loss and other non-operational factors, GlobalWafers 2022 EPS would have [ph] amounted to record-breaking high 40 per share. That would be a very good number.

So, what’s going on here? Why is Globalwafers holding significant amounts of shares in their competitor, Siltronic, leading to a meaningful impact on full year EPS?

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.