TSMC. How To Turn Chicken Salad Into Chicken Sh*t

TSMC. How To Turn Chicken Salad Into Chicken Sh*t

TSMC's shares have corrected ~8% despite beats, raises & unchanged FY24 outlook. Why?

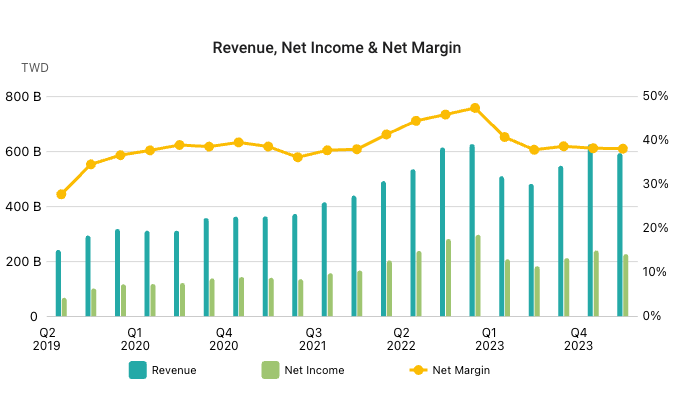

TSMC reported Q124 revenues of NT$592.64 billion. In US$ terms, this amounted to $18.87 billion, marginally above the high end of the guided range, up 12.9% YoY and down 3.8% QoQ. Gross margin for the quarter was 53.1%, bang in the middle of the guided range.

Looking ahead, the company guided the current quarter for $20 billion at the midpoint, up 6% sequentially. This was slightly higher than we had predicted earlier in the week in this earnings preview Multiple Positive Catalysts Ahead Of Q124 Earnings Season

The first quarter is typically TSMC’s weakest quarter based on simple seasonality. With that already up 16% YoY, it seems eminently feasible for the company to hit their low-to-mid 20% growth target for the year. Equally, it seems highly likely that they will guide the second quarter up sequentially. Looking at historical second quarter sequential growth rates, and stripping out some of the anomalous years, I think we can expect 3-5% QoQ growth for Q224. Let’s see on Thursday.

The company also took the opportunity to reiterate their full year growth forecast as unchanged from the previous quarter

Supported by our technology leadership and broad customer base, we expect that our business to grow quarter-over-quarter throughout 2024 and reaffirm our full year revenue to increase by low to mid-20% in U.S. dollar terms.

They explained that they had experienced minimal impact during the recent Taiwan earthquake, the country’s most powerful in twenty five years:

Based on TSMC's deep experience and capabilities in earthquake response and damage prevention as well as regular disasters drills, the overall tool recovery in our fabs reached more than 70% within the first 10 hours and were fully recovered by the end of the third day. There were no power outages, no structural damage to our fabs, and there's no damage to our critical tools, including all of our EUV lithography tools.

There was some impact however, and this will manifest itself as a 50 basis point impact on gross margin in the current quarter:

That being said, a certain number of wafers in process were impacted and had to be scrapped, but we expect most of the lost production to be recovered in the second quarter and, thus, minimum impact to our second quarter revenue. We expect the total impact from the earthquake to reduce our second quarter gross margin by about 50 basis points, mainly due to the losses associated with wafer scraps and material loss.

Personally, I think the way TSMC was able to cope with such a powerful earthquake is an amazing accomplishment. Judging by the market reaction after earnings, it would appear that this was completely overlooked.

As you might expect, and in case we might have forgotten, the recent surge in demand for all things related to AI acceleration will be a huge tailwind for TSMC for many years to come. The company expects AI-related revenue to double YoY in 2024, and will amount to low-teens percent of total revenue:

In summary, our technology leadership enables TSMC to win business and enables our customer to win business in their end market. Almost all the AI innovators are working with TSMC to address the insatiable AI-related demand for energy-efficient computing power. We forecast the revenue contribution from server AI processors to more than double this year and account for low-teens percent of our total revenue in 2024.

That’s a strong tailwind, but it’s going to get even stronger and grow at a 50% CAGR over the next five years, propelling it to >20% of revenues by 2028

For the next 5 years, we forecast it to grow at 50% CAGR and increase to higher than 20% of our revenue by 2028. Server AI processors are narrowly defined as GPUs, AI accelerators and CPUs performing training and inference functions and do not include the networking edge or on-device AI.

We expect server AI processors to be the strongest driver of our HPC platform growth and the largest contributor in terms of our overall incremental revenue growth in the next several years.

There was truly a lot of really good news in TSMC’s latest earnings call. Yet, the market reaction was decidedly negative and over the course of the following two US trading sessions, the stock has corrected by ~8%. What gives? Why was the reaction so negative? While some of it may be down to broader market sentiment, there was a strong element of TSMC shooting an own goal, creating confusion in the minds of investors and analysts alike. Here’s what we think of what TSMC said and how they could have handled the messaging a whole lot better.

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.