AMAT. Post Earnings Surge For No Good Reason

AMAT. Post Earnings Surge For No Good Reason

Still a great company with excellent growth prospects, just not in 2024

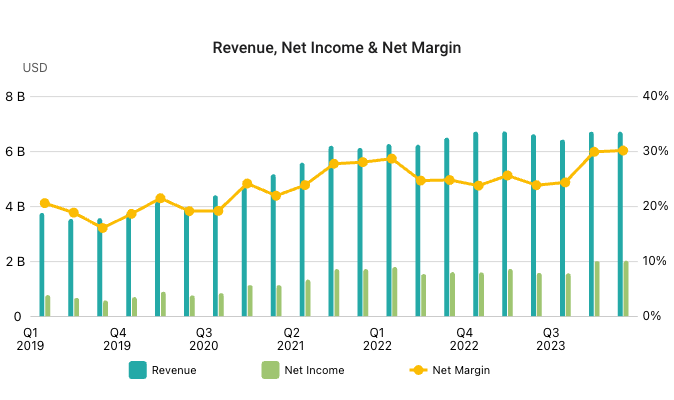

AMAT last week announced Q124 revenues of $6.71 billion, at the high end of the guided range and essentially flat sequentially both QoQ and YoY.

Commenting on the results, CEO Gary Dickerson noted the following:

“Applied Materials delivered strong results in the first quarter of fiscal 2024 and has outperformed our markets for the fifth consecutive year. Our leadership positions at key semiconductor inflections support continued outperformance as customers ramp next-generation chip technologies critical to AI and IoT over the next several years.”

In terms of current quarter guidance, AMAT is predicting $6.5 billion at the midpoint, a modest downward movement of 3% QoQ and in line with what we saw from peers KLAC and LRCX some weeks earlier.

Despite the results being largely in line with expectations, AMAT’s share price rallied strongly, increasing from ~$180 just prior to earnings to close the week at $199, having earlier pulled back slightly from an intra-day all time of $206.

We share our thoughts on what may lie behind this unexpected rally, discuss our concerns about AMAT’s exposure to the China market. We also dissect some of the key commentary from the earnings call, in particular, the company’s reluctance to provide any meaningful guide for full year 2024. Thanks as always for reading!

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.