AMD. With FY23 Revenues Set to Fall ~4% YoY, Is The Party Over?

AMD. With FY23 Revenues Set to Fall ~4% YoY, Is The Party Over?

Or is it just beginning?

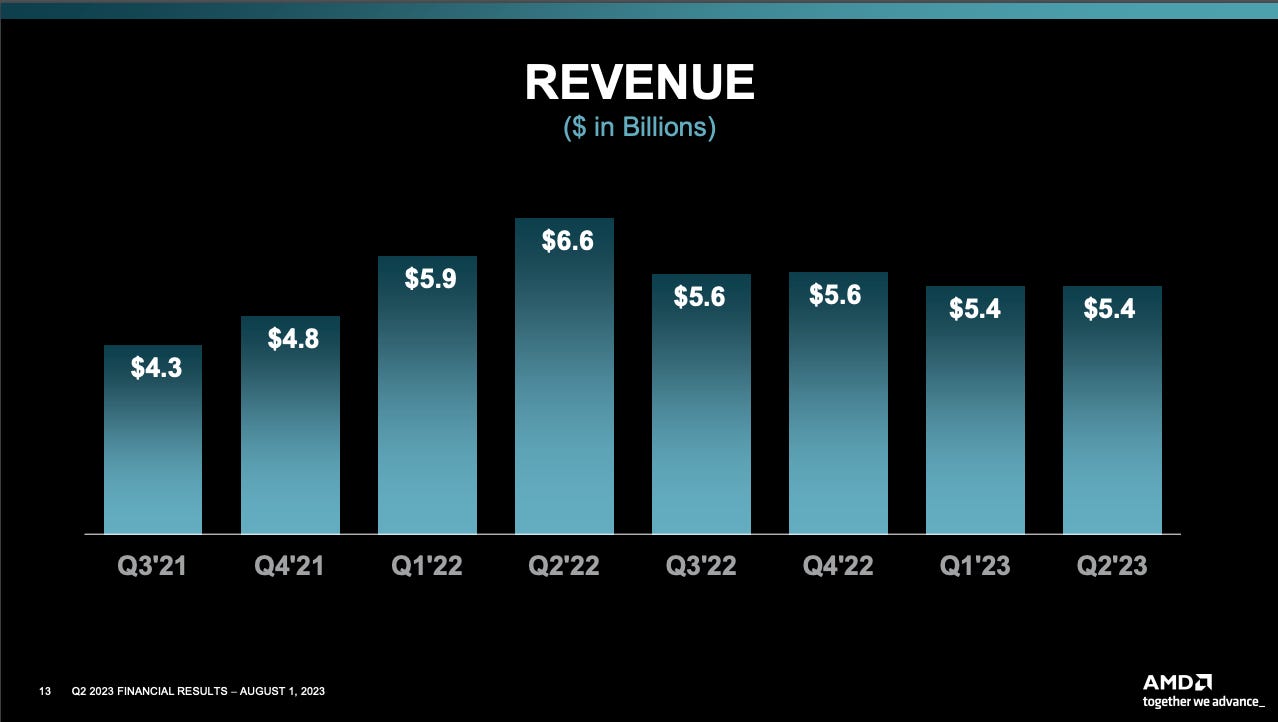

AMD’s resurgence against a dominant Intel saw the company grow annual revenues >4x between 2017 and 2022, excluding the roughly $3 billion added by the acquisition of Xilinx last year. Now, based on their current quarter forecast, FY 2023 revenue is likely to be down roughly $1 billion or ~4% YoY.

At the same time, AMD’s market share growth in the key server and notebook segments stagnated during the four quarters between Q322 and Q223.

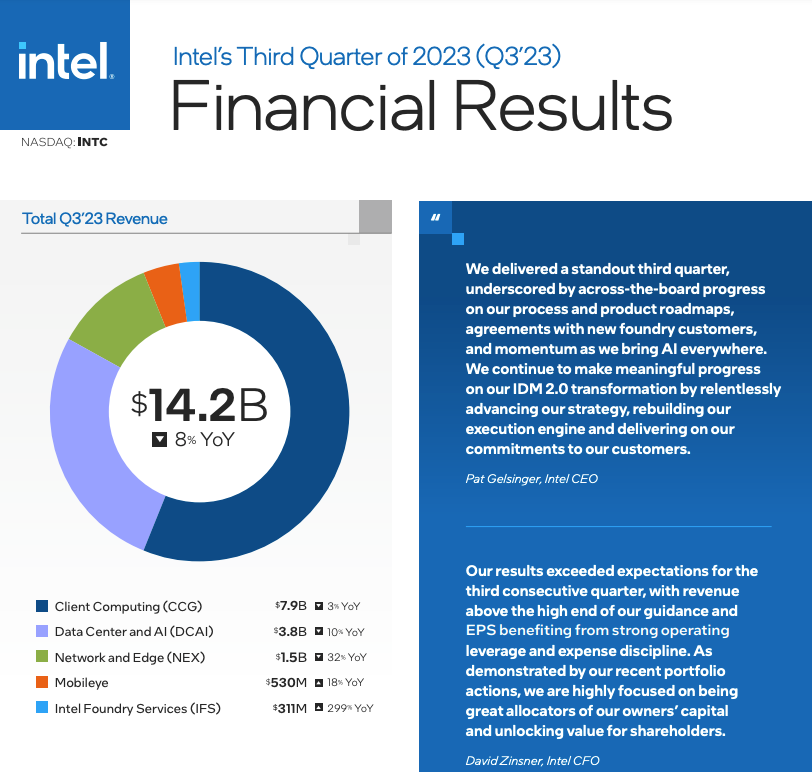

Meanwhile, Intel has not been standing still. The company claims that its “5 nodes in 4 years” strategy remains on track. Intel also maintains that its plans to compete in the foundry space are progressing well with some (as yet unnamed) customers already agreeing to prepay for access to their 18A node when it becomes available in 2025.

So, has AMD reached the end of the line in terms of its resurgence? That’s a complicated question. For our part, we’ve been documenting AMD’s remarkable turnaround for over five years now. One of our first pieces on the topic was the following, published in May 2018

Here’s our conclusion from the above piece:

Just as the hype surrounding the launch of AMD's zen-based products last year has subsided, the reality of what AMD can reasonably hope to accomplish is beginning to set in. While AMD would rightly consider that 2017 was an extremely successful year for the company, many investors were surprised that they had such little impact on Intel's market share in either client or server.

On the back of the strong 2017 and an even stronger Q1 2018, that situation may well be about to change. Firstly, on the client side, we expect that AMD will have largely completed the migration of its product lineup to Ryzen by the end of Q2. This will continue to drive increased revenues by virtue of the higher ASP's for Ryzen compared to the legacy product.

On the server side, AMD has been quite clear about their goal of achieving 5% market share by EOY 2018 and 10% in the "mid-term". With the company projecting a $21 billion data center TAM, that 5% would represent an additional $1 billion in revenues in 2018.

Furthermore, if Intel's 10nm delay persists, AMD's second-generation EPYC based on TSMC's 7nm process would become an even more attractive proposition for enterprise data centers. In conclusion, Intel may have unwittingly made it easier for AMD to gain a foothold in the very market they most want to protect.

At the time of that writing, AMD’s share price was around $10. If that sounds ridiculously low in comparison to its price today of around $139, you would need to keep in mind that back in 2015, you could have purchased AMD for around $1.50

Along the way, AMD’s resurgence had some ebbs and flows, albeit mostly flows. We documented an important milestone in AMDs comeback the following year in this article:

In our opening remarks, we noted the following:

Yet, this same period saw the company's stock fall by almost 18% on the back of a weaker than expected full year outlook coupled with broader market uncertainties related to trade wars and an increasingly gloomy global economic growth outlook. Despite this setback, we remain convinced in our view that the best is yet to come for AMD. Here's why.

For some context, in the six months prior to writing this piece, AMD’s share price had corrected from just north of $14 to around $9.50. Many thought that this was the end of the line for AMD. When 2019 came to a close, revenues had grown just 4% YoY.

As we now know, 2019 was simply a hiatus. In the years that followed, AMD went from strength to strength, until this year. In many ways, AMD’s performance in 2023 resembles what happened back in 2019. Just like we predicted back then, that was really just the beginning for AMD. The same remains true today. Here’s why….

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.