Applied Materials ICAPS Grows Strongly But Leading Logic Ruins The Party

Push outs and cancellations spread to leading logic. Ouch!

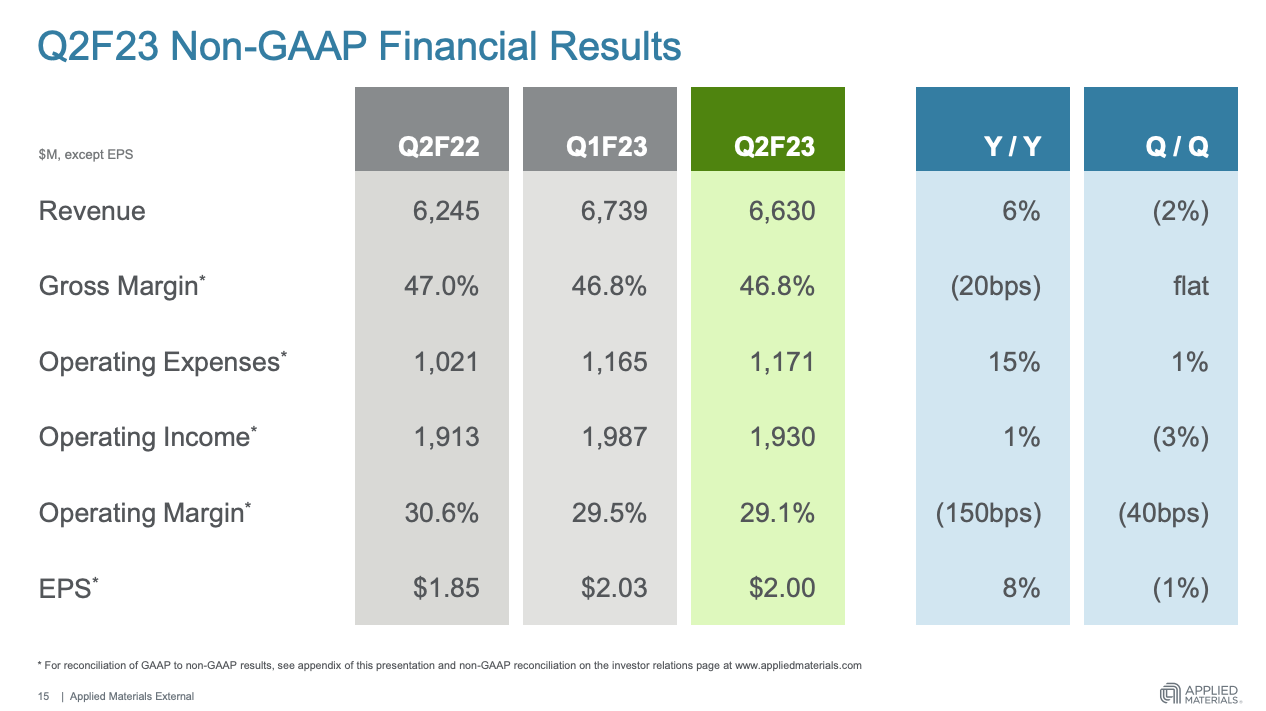

AMAT reported Q1’23 revenues of $6.63 billion, up 6 % YoY, down 2% QoQ and modestly above the midpoint of the guided range. Non-GAAP gross margin was flat sequentially at 46.8 percent, operating income of $1.93 billion and EPS of $2.00.

With the exception of ASML, AMAT’s Q1’23 results are in stark contrast with their peers, most of whom had significant sequential declines in revenue. Their closest US peer, LRCX, was down 26.7% sequentially for example.

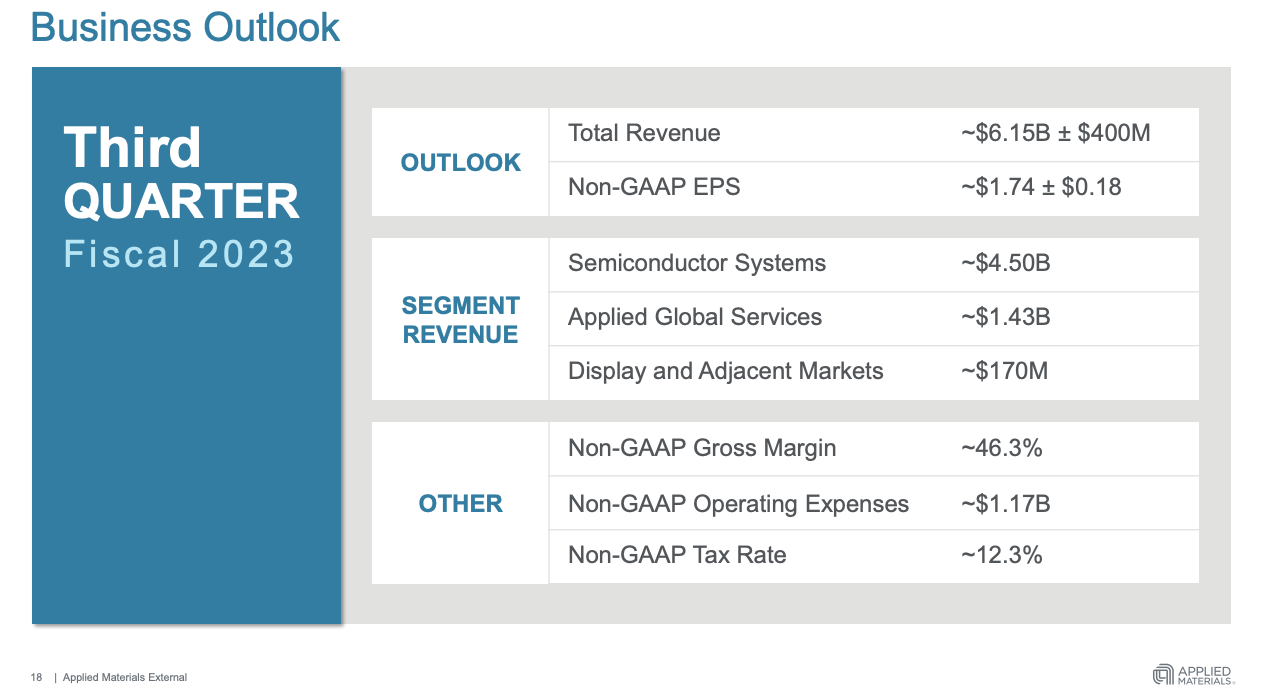

Looking ahead, AMAT forecasted current quarter revenues of $6.15 billion at the midpoint, down 7.2% QoQ. The lion’s share of that decline will be in their Semiconductor Systems segment:

Why were AMAT able to outperform to such a significant level last quarter? Why now are they just now forecasting a meaningful sequential revenue decline, albeit less than their peers? Let’s dig in ….