ASML Q425. Employees Asking For Headcount Reductions? Give Me A Break!

something has spooked the company into making drastic headcount reductions

ASML this week reported Q425 revenues of €9.7 billion, €200 million above the guided midpoint, up 30% QoQ and up 5% YoY. It was the company’s highest ever quarterly revenue, easily eclipsing the previous record high on €9.2 billion back in Q424.

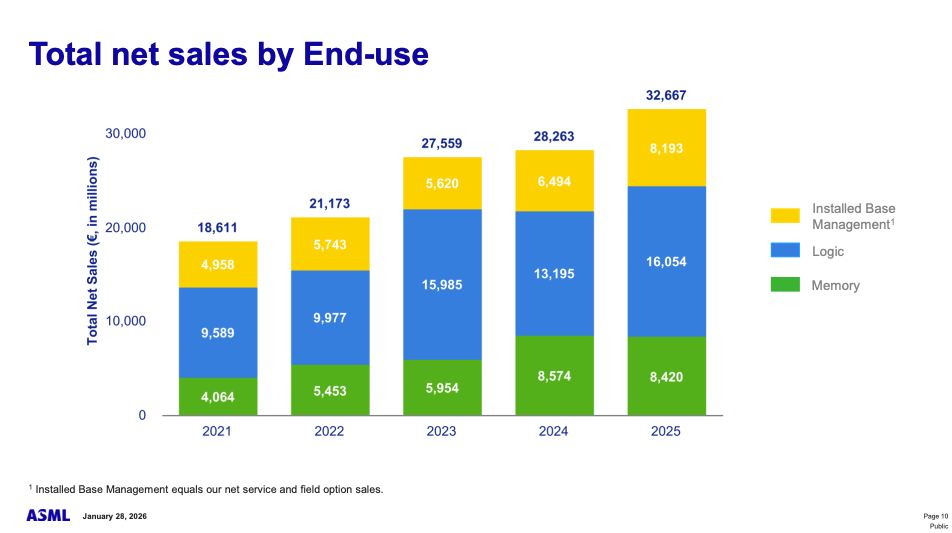

Gross margin for the quarter came in at 52.2%, in line with guidance. For the full year 2025, revenues amounted to €32.7 billion, representing a 16% YoY increase.

As can be seen from the above graphic, net sales allocated to memory in 2025 amounted to €8.4 billion, slightly down YoY. This is perhaps one of the best ways in which to view the current memory shortage. What do I mean by this? Well, using ASML as a proxy for all CapEx spending by the memory makers, this reflects their strategy of minimising wafer capacity growth and focusing primarily on technology transitions. Judging by the current share prices for the likes of MU, WDC, SNDK, SK Hynix etc, it would appear to have been a very successful strategy if measured by that yardstick.

ASML’s CEO Christophe Fouquet and CFO Roger Dassen were noticeably upbeat in their remarks on the earnings call, in particular highlighting a growing confidence in the sustainability of AI-drive investment

Clearly it was a strong quarter. It was a record quarter in terms of revenue. It was a record quarter in terms of order intake. It was a record quarter in terms of free cash flow generation. So from that vantage point, clearly a very strong quarter.

If you listen to our customers, both what they say publicly, but also what they told us, it's pretty clear that customers over the past couple of months have actually become more positive in their assessment of the medium-term market perspectives as they see it. I think it's primarily on the basis of the more robust view that they have when it comes to demand for AI, which seems to be more sustainable from their vantage point. That recognition has led some of our customers to really invest in capacity and gear up their plans for medium-term capacity expansion. So that's been clearly the case.

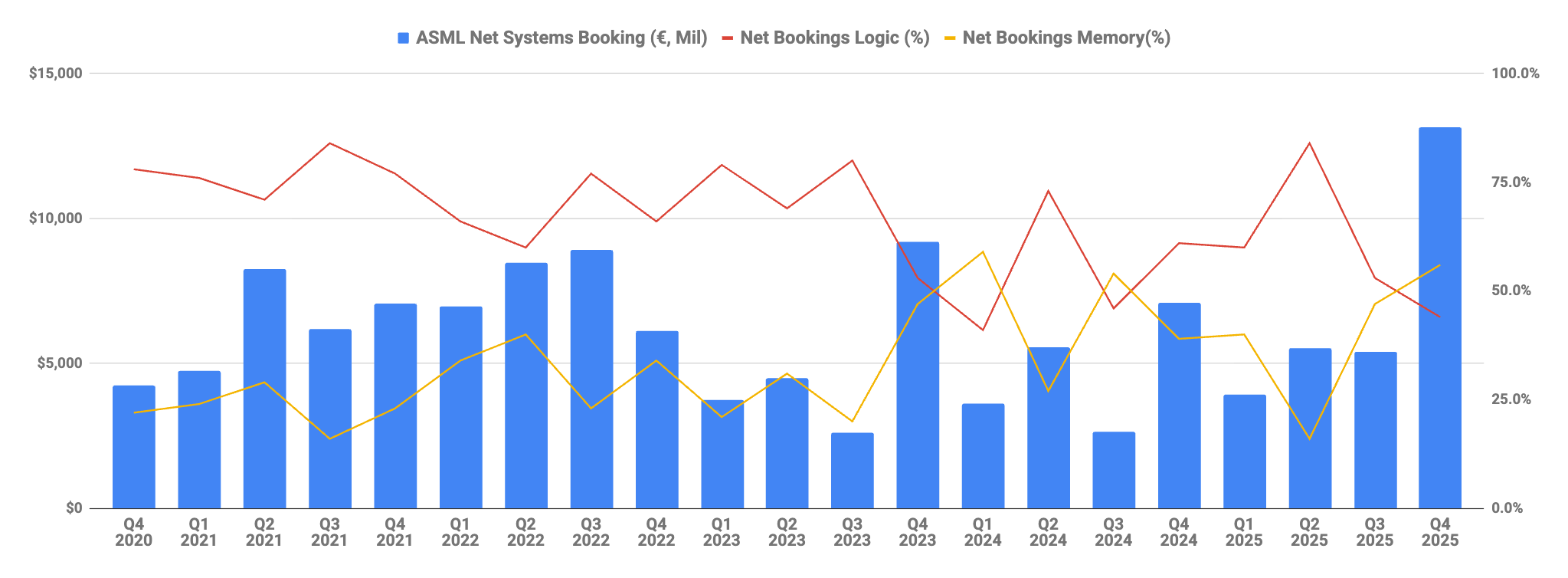

Here, they are clearly referring to what we heard from TSMC on their earnings call two weeks ago. More specifically, a meaningful chunk of the significant increase in TSMC’s planned 2026 CapEx will likely come ASML’s way and this translated into their largest ever end of quarter net bookings by far at €13.2 billion, of which €7.4 billion is slated for EUV tools.

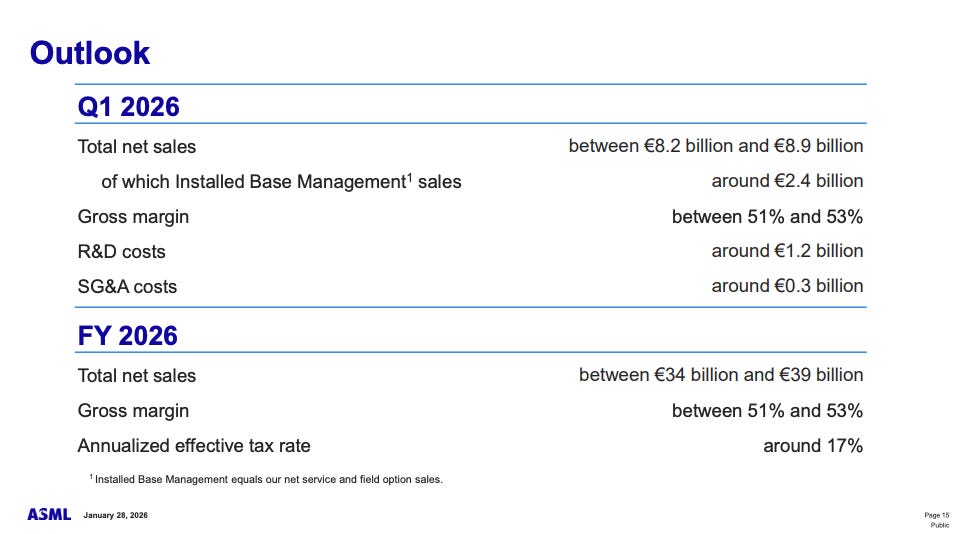

For the current quarter, the company expects revenues of €8.55 billion at the midpoint, with gross margin remaining flat to the prior quarter.

For the full year 2026, ASML forecasted revenues of €36.5 billion at the midpoint, representing an 11.6% YoY growth. In the initial aftermath of the earnings call, ASML’s share price rose modestly in premarket trading, up around 5% at one stage. However, those gains were reversed during the actual session and the share price closed down ~2% on the day.

I think it would be unwise to read to much into this share price action given the fact that ASML is up over 100% in the last six months. However, a number of details on the earnings call did give me some food for thought.

#1 Long term outlook unchanged

#2 End of year backlog lower than might have been expected

#3 Declining sales to China

#4 Out of the blue job cuts announcement

Of these four points, the last is the most concerning. While the headline number of 1,700 positions being axed sounds bad, it’s represents just 4% of their total workforce. For some context, technology companies consistently trim their workforces by this amount through their annual review process mechanisms. As a manager at Intel, it was business as usual for me to have a 5% target for “improvement required” ratings each year, these normally being the first step in what would ultimately result in a termination.

This begs the question, why does ASML leadership see fit to make a high profile announcement of this sort? According to the CEO, this headcount reduction is driven not by needing to cut costs, rather by feedback from their employees and from their customers that the organization has become too complex, impacting decision making and responsiveness. Employees asking for their headcount to be slashed? Seriously? What’s really going on here? Let’s dig in…