China Semi Foundry: Fierce Competition & Sluggish Rebound In Year Of The Dragon

China Semi Foundry: Fierce Competition & Sluggish Rebound In Year Of The Dragon

China's two leading foundries have ~80% domestic dependence. Right now, that's a headwind

Now that both Taiwan & China’s leading foundry players have reported Q423 earnings, a clearer picture is emerging with regard to what we can expect from foundry in 2024.

TSMC set the stage back in mid January with their forecast for foundry revenue to grow 20% YoY and they would grow more. Interestingly, that confidence has not been echoed by their much smaller peers. UMC declined to provide any full year forecast, SMIC is expecting mid-single digit growth while Hua Hong is basically just saying that 2024 will be better than 2023. Go figure! Of course we still await Globalfoundries report, due on February 13. Will be interesting to see what they have to say.

In terms of SMIC and Hua Hong earnings, I’ll spare you the boring details. Basically both reported Q423 revenues in line with expectations and both guided essentially flat to slightly down for Q124.

One thing both companies had in common in Q423 was a significant decline in gross margin QoQ. This had previously been flagged on their prior quarter report, so there was no surprise. However it’s still worth a mention here. On their call, Hua Hong broke down the components of the gross margin decline from ~16.1% in Q423 to 4% in Q424 as follows:

10% points due to ASP decline

3.9% due to “inventory provision”, meaning, one presumes, writing down to some meaningful degree, the value of inventory on hand.

We don’t know the extent of the ASP decline, but while unit shipments declined just 5% QoQ, revenues declined ~20%. By my calculations, that works out at a roughly 10% ASP decline QoQ.

With gross margin at 4%, one would anticipate a negative net income, of greater magnitude than the net loss of $12.8 million in Q323 when gross margin was 16%. But you would be wrong. An “Other income” line item of $87 million, aka government subsidy, brought the company to a positive net income of $3.5 million.

The bottom line is that it was a terrible quarter for Hua Hong, one that was perfectly forecasted, but terrible nonetheless.

Looking ahead, Hua Hong was adamant that thing were on an improvement trend for the current quarter and beyond. Here’s some quotes from the earnings call:

Booking getting stronger over past two months, esp CIS & PMIC. Pretty strong demand for these two areas. Weakness in power discrete, esp IGBT super junction. Not worried about this. Expect recovery after CNY. MCU is still weak. Expect this to gradually improve. Pricing has stabilised. Q423 was the trough.

Goal is to get loading to 95% to 100% by end of June. Very good chance to achieve that. Bookings for certain segments are strong. MCU will gradually recover. Once we get higher utilization for 12 inch fab. Then we can improve pricing for different technology platform. Then we will see a gradual improvement in gross margin.

We believe we hit the bottom in Q4. Stabilised over the past two months. Strong bookings for some segments. Recovery of smartphone market, strong demand for the AI market. Pricing stabilised in Q1.

Good chance that all segments will recover in the second half. Let’s keep our fingers crossed.

Fingers crossed indeed!

Another thing that caught my attention in SMIC’s earnings press release was the following commentary in relation to the business climate that prevailed for 2023 as a whole:

Unaudited profit attributable to owners of the Company was $902.5 million in 2023, a decrease of 50.4% from $1,817.9 million in 2022. The main reasons were: over the past year, the semiconductor industry was at the bottom of the cycle. Demand in the global market was weak. Industry inventories were in high level, with slowing down of de-stocking. The competition within the industry was fierce. As a result, the Group’s average capacity utilization rate declined, wafer shipment decreased and product mix changed. In addition, the Group was in high investment period, and depreciation increased accordingly compared with 2022. The above factors together impacted the Group’s financial performance in 2023.

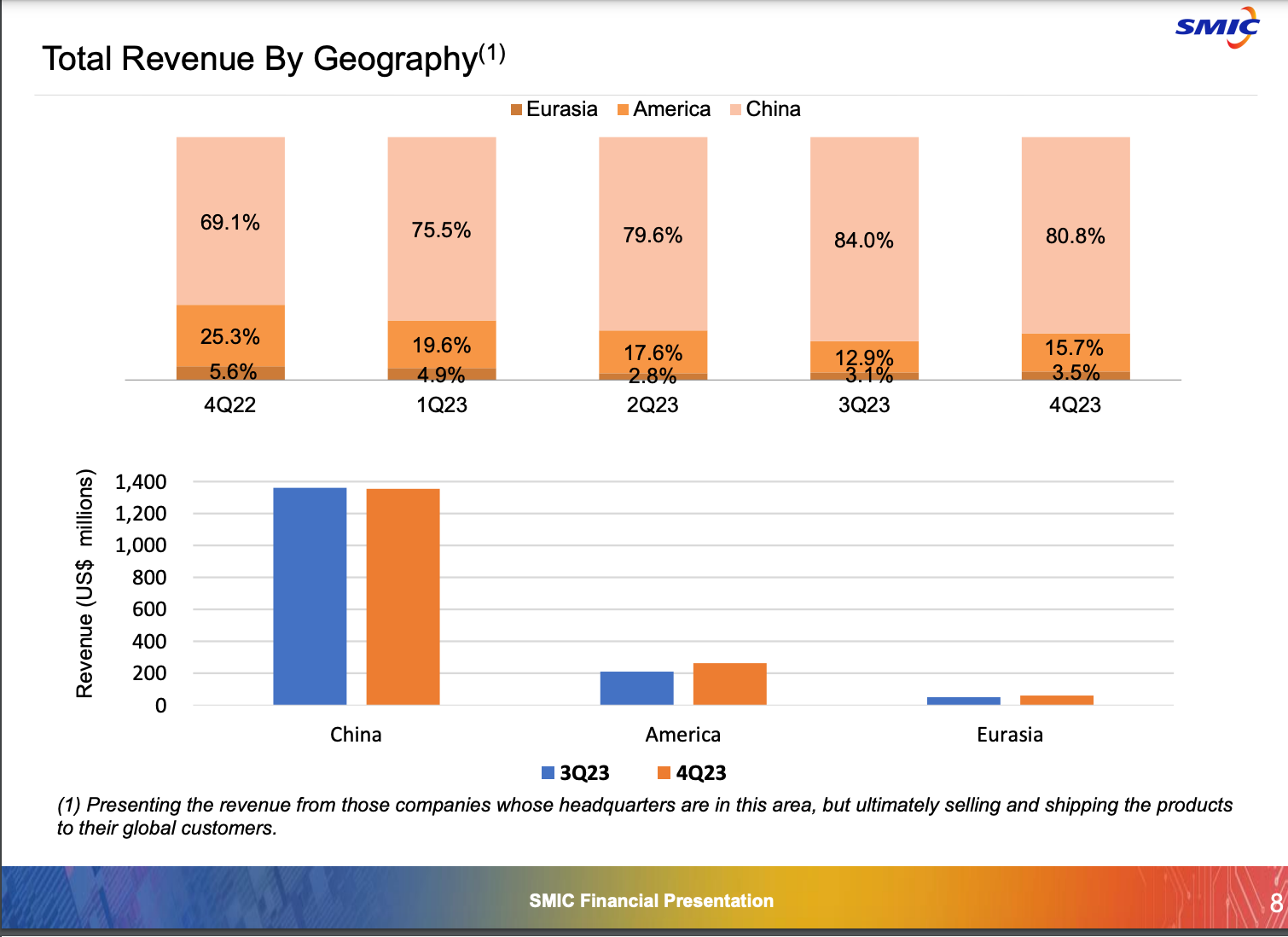

I’ve highlighted the sentence on competition being fierce. This is quite a dramatic statement. Of course, the foundry business is nothing if not competitive. However, one gets the sense that this comment refers to competition within China. After all, ~80% of SMIC’s revenues are generated in China:

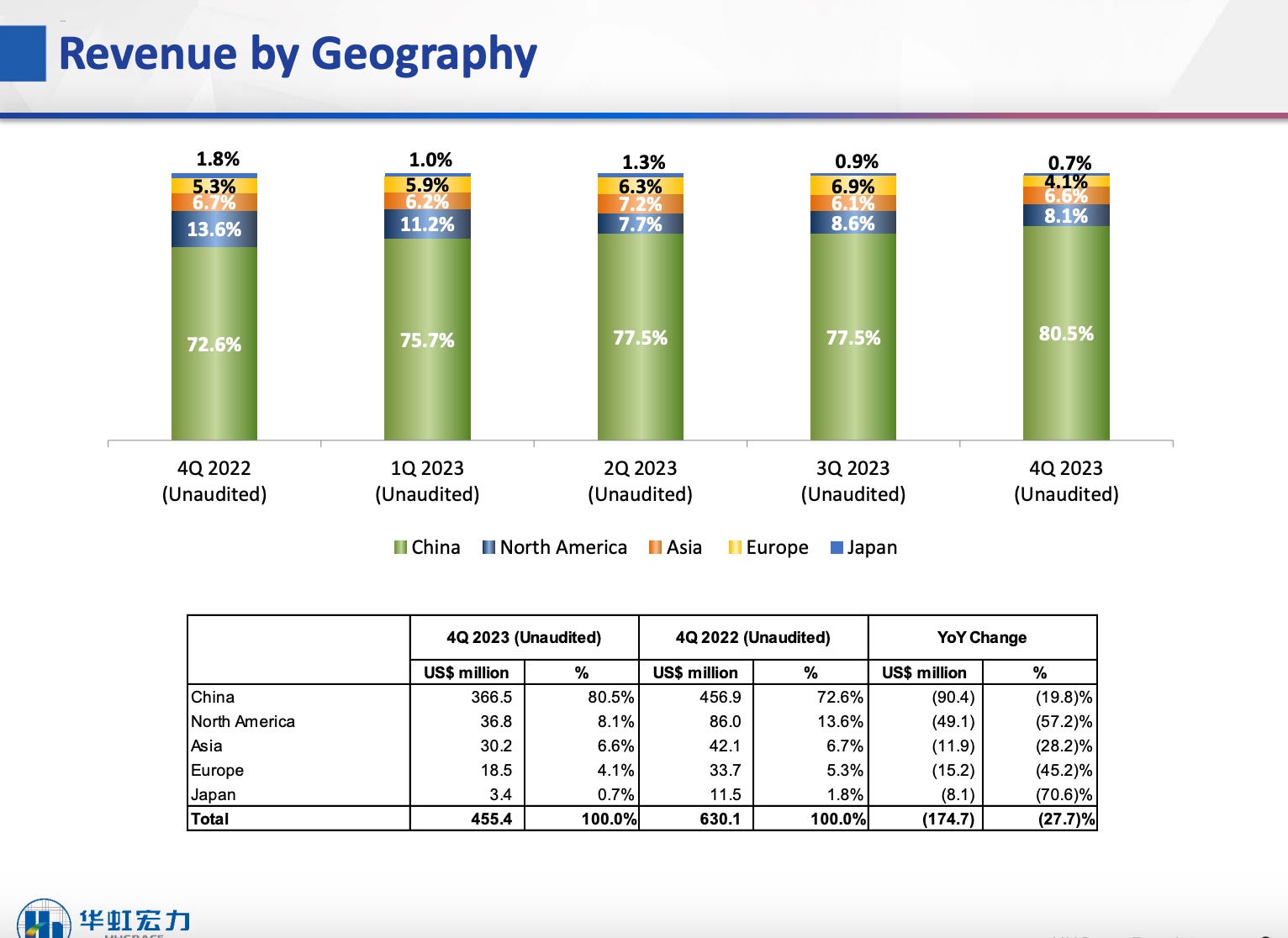

It’s a similar story for Hua Hong. From 72% in Q422, their China sourced revenue was also at 80.5% in Q423:

Our thoughts on this huge over reliance on the domestic market and the fierce competition therein, the prospects for China foundry in 2024 and beyond together with our views the attractiveness of the segment from an investment perspective.

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.