Globalfoundries. Pressure Grows As Customer Penalties Soar

SMIC will outspend GFS 10x CapEx in 2024

Globalfoundries (GFS) reported Q423 revenues of $1.854 billion, marginally above the midpoint of the guidance range, down 12% YoY and essentially flat sequentially.

It’s interesting to note that, throughout 2023, while GFS’s quarterly revenues were essentially flat, they did actually increase by a few million dollars each quarter. Could they possibly have engineered this just so that they could refer to having grown QoQ each quarter?

More on that to come, but let me first discuss the highlights from our fourth quarter 2023 results, which Dave will comment on further. Revenue in the fourth quarter increased sequentially to $1.854 billion, which was above the midpoint of our November provided guidance range.

Yes, the sequential increase was by $2 million, or 0.1% Personally, I’d just call it flat QoQ and leave it at that :-)

Adjusted gross margin for the quarter was 29% , at the upper end of our guidance range and flat sequentially:

It’s quite remarkable how consistent both quarterly revenues and gross margin have been through the downturn for GFS. This is actually quite an important point to note, and we shall return to it later.

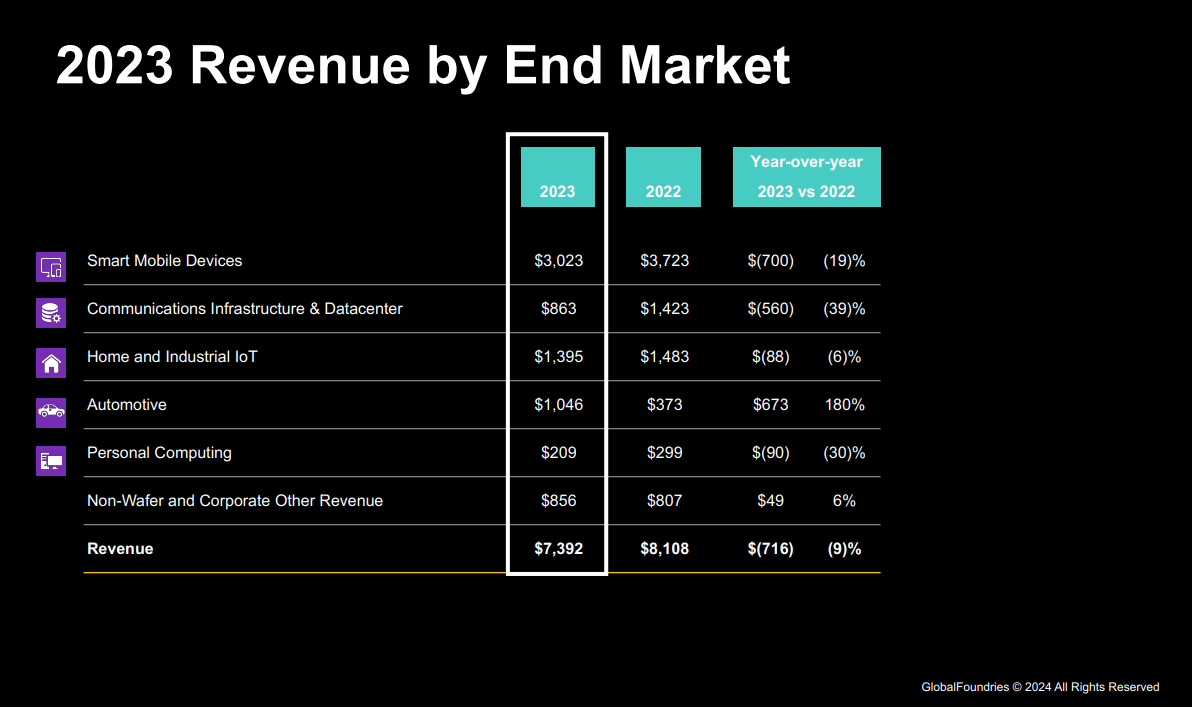

For 2024 as a whole, GFS revenue declined by 9% YoY to $8.1 billion while wafer shipments fell 11% YoY to 2.2 billion 300mm equivalents.

This was a pretty respectable performance from GFS in what was a very challenging year for the foundry segment. Taiwan’s UMC, for example, saw their 2023 revenues decline by 20% YoY while China’s SMIC recorded a 13% drop YoY.

While 2023 was certainly a difficult year for GFS, there was one particularly bright spot that we should pay attention to, namely Automotive.

While Coms Infrastructure & Data Center declined by 39% and Smart Mobile Devices by 19% YoY, their Automotive segment grew by 180% YoY to reach just over $1 billion. While there was certainly a slowdown in Automotive in H223, it still delivered QoQ growth of 5% in Q423.

The problem child for GFS is its over reliance on the Smart Mobile Device segment. In 2022, this segment accounted for 46% of overall company revenues, falling to 41% in 2023. The main problem with this segment in 2023 was the decline in unit shipments which we recently discussed here 2023 PC Unit Shipments Disappoint While Smartphone Fared Better Than Expected:

For 2023 as a whole, Smartphone unit shipments amounted to 1.17 billion units, representing a 3.2% YoY decline, far better than we expected at the beginning of last year.

It might seem odd that a 3.2% decline in Smartphone unit shipments could result in a 19% YoY decrease in revenues for GFS. The explanation, I think, is that GFS is largely playing in the Tier 2 smartphone segment. Indeed, the premium smartphone segment experienced quite a good year in 2023 and GFS is trying to pivot towards greater exposure there:

To partially offset these dynamics, we continued to remix our business towards the premier tier of the handset market, where demand levels and average selling prices per wafer have remained resilient.

Furthermore, there’s a tailwind in the offing for GFS as more and more Tier 2 smartphones adopt 5G in the years ahead. Probably not much impact in H124, but should be more noticeable in H224.

Guidance

As the last of the major global foundry players to report earnings, GFS’s guidance was highly anticipated. In our review of their Q323 earnings call three months ago, we speculated on what was likely in the pipeline…

GlobalFoundries Pops On Q323 Earnings. But Why?

GlobalFoundries reported Q323 revenues of $1.85 billion, flat sequentially but down 11% YoY. Net income was $249 million, up 5% sequentially but down 26% YoY. At 28.6%, gross margin was essentially flat sequentially. Basically all key metrics were modestly to the high side of the guided numbers.

Our conclusion back then was as follows:

#1 There will be further underutilisation penalties in Q423, likely higher than they were in Q323

#2 As the LTAs are negotiated for 2024 between now and December 31, its highly likely that their customers will opt for lower wafer volumes for multiple reasons but mainly because they know that GlobalFoundries has significant underutilised capacity which they can bring back online at short notice. So why take the risk and over order and possibly incur penalty payments yet again.

As we move from a bruising 2023 into an as yet unknown 2024, the LTA bargaining power will tilt in favour of GlobalFoundries customers. Based on their “True Up” comments, distinctly downbeat outlook and >50% 2024 YoY CapEx cut, it feels to us like the company is laying the groundwork for a significant downward guide when they report Q423 earnings in early February 2024. Let’s see.

The underutilization penalties were indeed higher as we predicted, and we shall discuss this in more detail later. In the meantime, GFS declined to provide a full year 2024 guidance but had this to say about Q124:

Now let me provide you with our outlook for the first quarter of 2024. We expect total GF revenue to be between $1.5 billion to $1.54 billion. Of this, we expect non-wafer revenue to be approximately 11% of total revenue. We expect gross profit to be between $345 million and $385 million. We expect operating profit to be between $120 million and $180 million.

At the midpoint of $1.52 billion, this represents a sequential decline of 18%. To make matters worse, Gross Margin is set to decline from 29% in Q423 to 23% in Q124:

So, what’s going on here? GFS QoQ decline of 18% is far greater than any of their peers. Why is their gross margin falling far below their run rate through 2023? What penalties did they impose on their customers during the prior quarter? What was the mood music on the earnings call and what can we predict about how 2024 is likely to shape up for GFS? Lastly, CEO Thomas Caulfield had some very interesting comments on the build up of WFE capacity in China, as well as on the recently announced Intel/UMC partnership. Let’s dig in…

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.