Intel Q1'23 Earnings Review. No Surprises But Pay Attention To The Gross Margin Story

Intel Q1'23 Earnings Review. No Surprises But Pay Attention To The Gross Margin Story

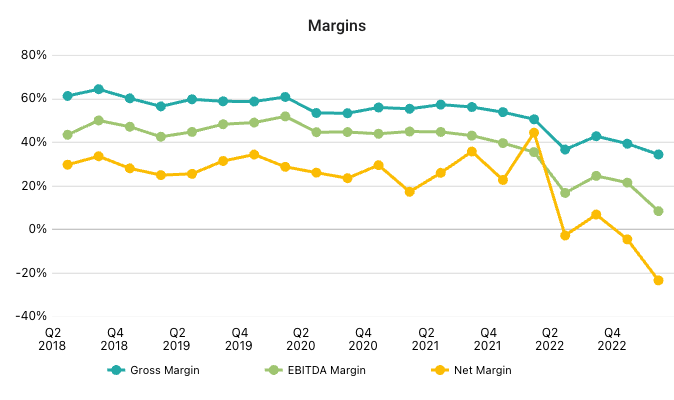

Annual GAAP GM has fallen from 61.4% in 2018 to 42.3% in 2022. But why?

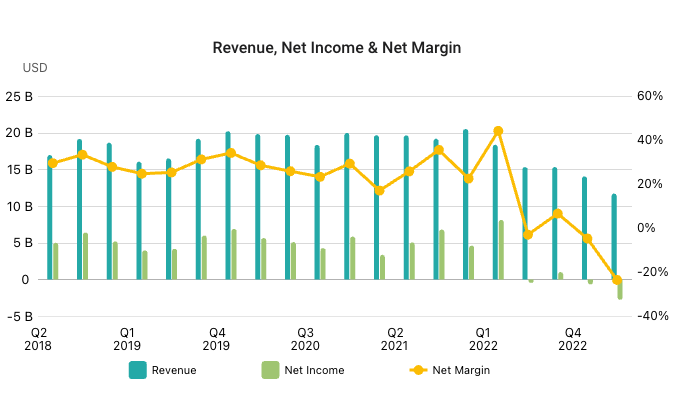

Intel last week reported Q1’23 revenues of $11.7 billion, down 37% YoY and 16.5% sequentially. However, at $700 million above the midpoint of the guided range from back in January, it was the first earnings beat recorded by the company since Q1’22.

At 38.4%, non-GAAP gross margin was down 14.7 points YoY and down 5.4 points sequentially.

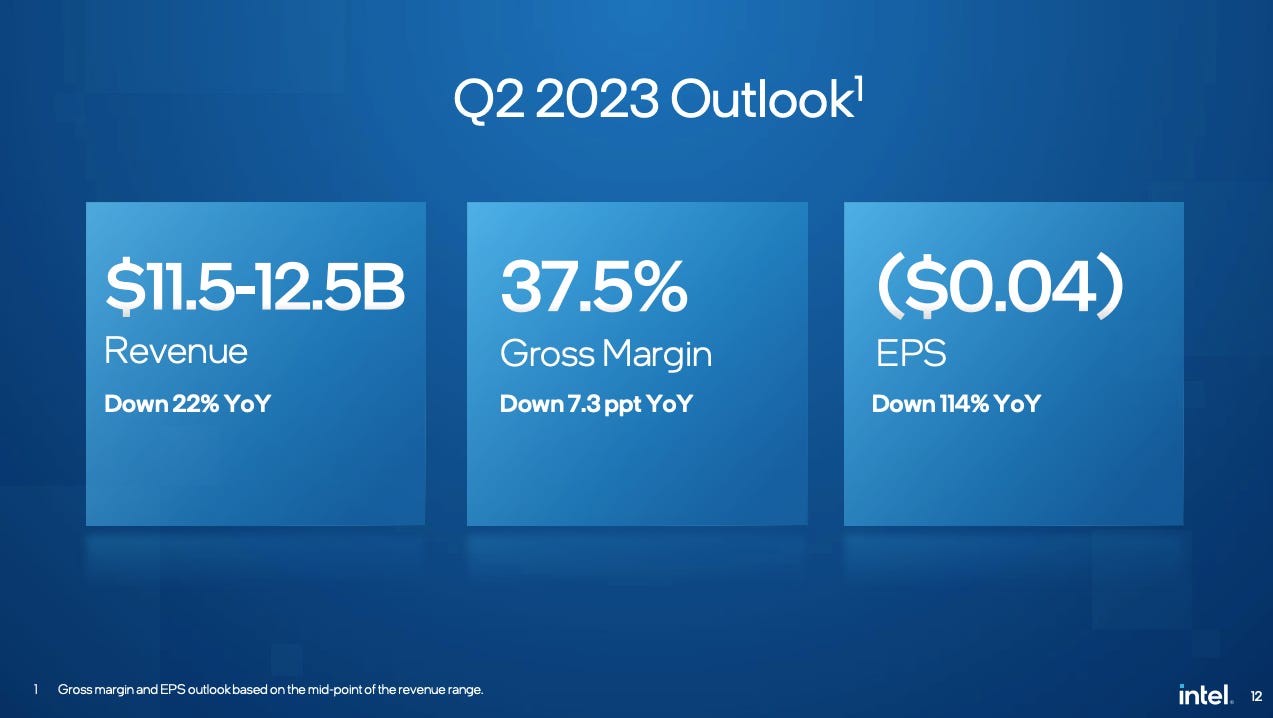

Looking ahead to the current quarter, Intel forecasts revenue of $12 billion at the midpoint, with non-GAAP gross margins sliding a further 0.9 points to 37.5%

CFO David Zinsner outlined some of the reasons driving the “unacceptably low” margin number:

Factory under load charges are projected to impact Q2 gross margins by approximately 300 basis points. While gross margins are well below acceptable levels, I'd highlight inventory reserves on pre-PRQ products impact Q2 margins by approximately 250 basis points, costs, which should begin to unwind later this year as new products launch. Increased sample costs in support of our Xeon product road map will impact margins by 40 basis points sequentially.

Note that the under loading impact was also 300 basis points in the first quarter, indicating that Intel’s fabs will remain at the same levels of utilisation QoQ.

Operating cash flow in Q1 was negative $1.8 billion, but with net CapEx spending at $7 billion, this lead to an adjusted free cash flow of a whopping negative $8.8 billion.

While Intel declined to give a specific CapEx forecast (or revenue forecast) for the current year, Zinsner did indicate that it would remain at levels similar to 2022, i.e. in the low 30% of revenue range:

We'll continue to deploy factory capacity prudently as we operate within our smart capital framework. As communicated last quarter, we expect to manage net CapEx intensity in the low 30% of revenue range in 2023, with capital offsets of approximately 20% to 30% of gross CapEx. Consistent with smart capital, IFS capacity represents approximately 10% of 2023 gross CapEx, a number which will scale in line with foundry customer commitments.

For the record, Intel’s CapEx in 2022 was $24.8 billion, up from $18.7 billion in 2021 and $14.3 billion in 2020.

Circling back to the gross margins, the topic featured prominently on the earnings call, meriting a total of 16 separate mentions. This is not that uncommon. In fact, on the Q4’22 earnings call, there were 21 separate mentions of “gross margin”. By way of contrast, “gross margin” merited 11 mentions on the latest TSMC earnings call.

Why is gross margin such an important topic on Intel’s earnings calls? Why do Intel CFOs (at least in recent years) have to spend so much time explaining what’s happening with the company’s gross margins?

The reason is simple. Intel’s gross margin trajectory (downwards) and their plans for how to revise it upwards over the coming 3 years is actually a reflection of a reality Intel does not want to publicly admit to or discuss. However, it’s a reality that every investor should be keenly aware of. Let’s dig in….

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.