Intel's New Segment Reporting. Transparency Or Obfuscation?

If it was launched a day earlier we could have written it off as an April Fool's joke...

Intel’s long-awaited new segment reporting structure was rolled out this week in the form of a webinar attended in person by a small number of hand-picked analysts. It’s worth taking a look at the webcast, if just to observe the body language of Mr. Gelsinger and Mr. Zinsner alone. This particular snapshot occurs around 32 minutes into the video as both men listen to the first question in the Q&A segment. They kinda remind me of two school kids brought into the principal’s office for a dressing down. Note how they play with their fingers. I wonder what that signifies?

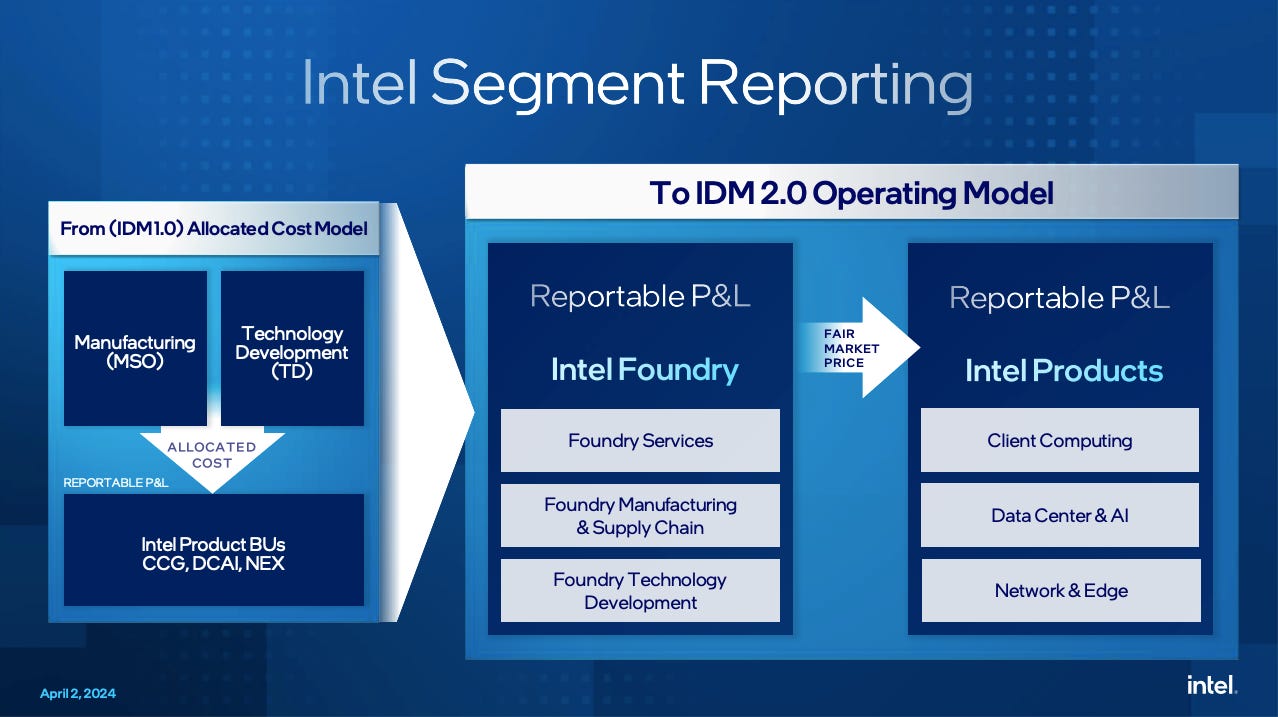

But I digress. In a nutshell what Intel has done is to reframe the way it looks at, and externally reports, itself, as outlined in the following graphic:

This is pretty much exactly what was expected, based on previous updates from CFO David Zinsner. As a result, rather than looking at numbers like this:

We shall look at numbers like this:

Note: the above is taken from the 8-k SEC filing made on the same day as the webinar and you can find that here.

It should be noted from the outset that Intel’s reallocation of numbers according to their new financial reporting structure is entirely within their own control, i.e they get to decide how big the Foundry P&L operating losses are.

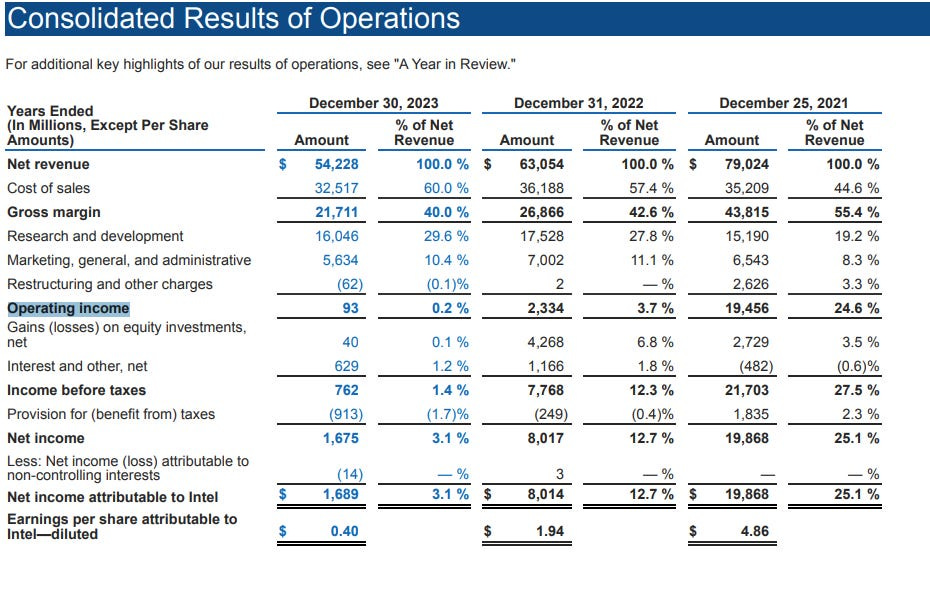

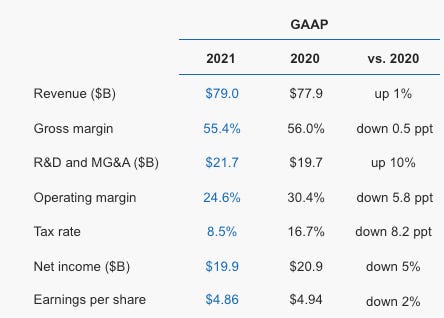

Here, it’s helpful to frame the discussion based on Intel’s results back in 2021 since this is the first of the three years included in the restatement of financials. That year was a record-breaking year for Intel, following hot on the heels of another record breaking year in 2020. Here’s a summary from the Intel Q4 2021 earnings release:

Net income was a whopping ~$20 billion, down just 5% on the previous year. Note that Gross Margin was 55.4%, down just 0.5 points YoY. Against this backdrop, Intel now tells us that looking back at 2021, the newly constructed Foundry P&L actually had an operating loss of ~$5 billion. Fair enough, if you say so, but who really cares?

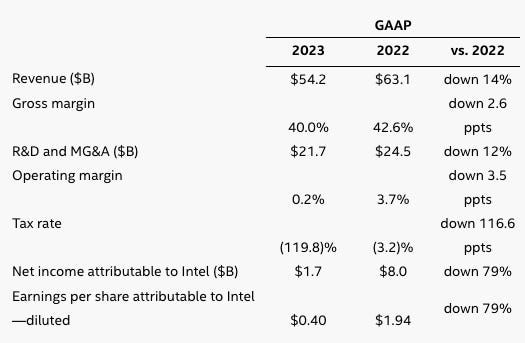

If we fast forward to 2023, and look at the Q4 2023 earnings release for comparison purposes, we get the following:

Revenue has obviously declined significantly compared to 2020/2021, a result of a combination of factors including divestitures, the global semiconductor downturn, a collapse in PC unit shipments and a ~18% YoY decline in server unit shipments.

But the bigger issue here is gross margin- it has collapsed from 55.4% in 2021 to just 40% in 2023. Keep this in mind, we shall return to this fact later. For the moment however, have a think about this: According to Intel, all process related issues have been fixed, the 5N4Y strategy is resolutely on track, the new nodes have been released on schedule, right? So why is gross margin heading south? Shouldn’t it be improving or at least close to stable, given that process technology is no longer an issue?

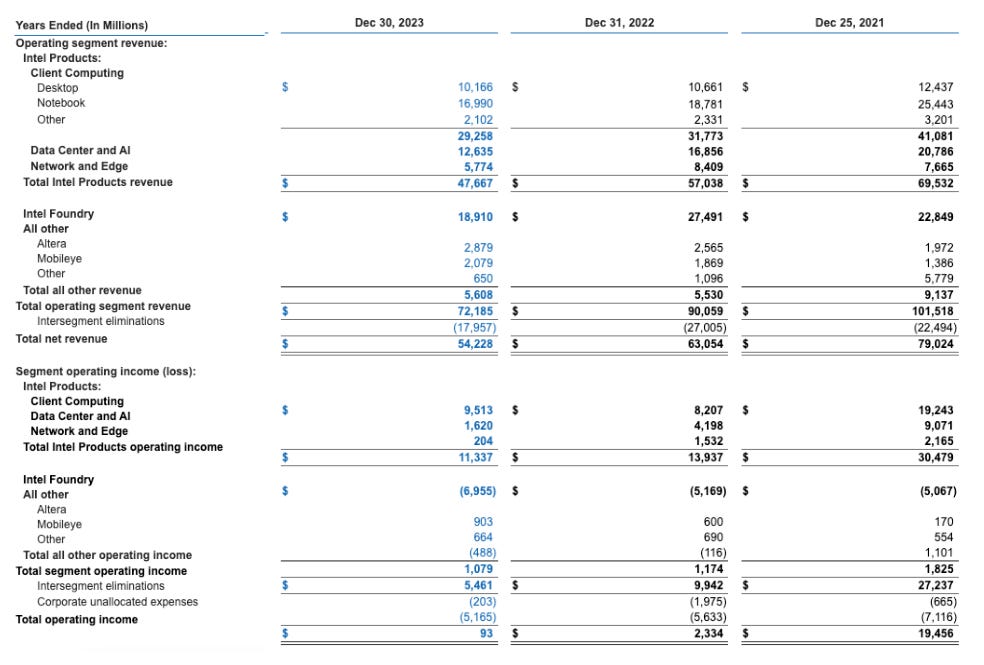

Back to the new financial model. As had been well telegraphed in advance, the Foundry P&L drew the short straw and has now been exposed as generating operating losses of >$17 billion over the course of the past three years. Curiously, this is not too far off the roughly $20 billion Intel stands to gain from the US CHIPS Act funding. No doubt, the US administration will be quietly bemused by the extent of the loss making that their benevolence will be helping to stem over the course of the next three years. It’s really a good thing that this financial restructuring was scheduled for after the CHIPS funding celebrations two weeks ago.

Before we dig further into the new reporting structure, we noted something quite amusing in the breakdown of the “Corporate unallocated expenses” line item from the above report, while scanning through the 8-k filing:

Notice how share-based compensation has increased from ~$2 billion in 2021 to ~$3.2. billion in 2023, a 50% increase? Investors will surely be delighted to know that the team that brought Intel down from ~$20 billion net income in 2021 to around $1.7 billion in 2023 paid themselves an extra $1 billion in the process. One would have to wonder that they would pay themselves in the unlikely event that they actually increased net income…

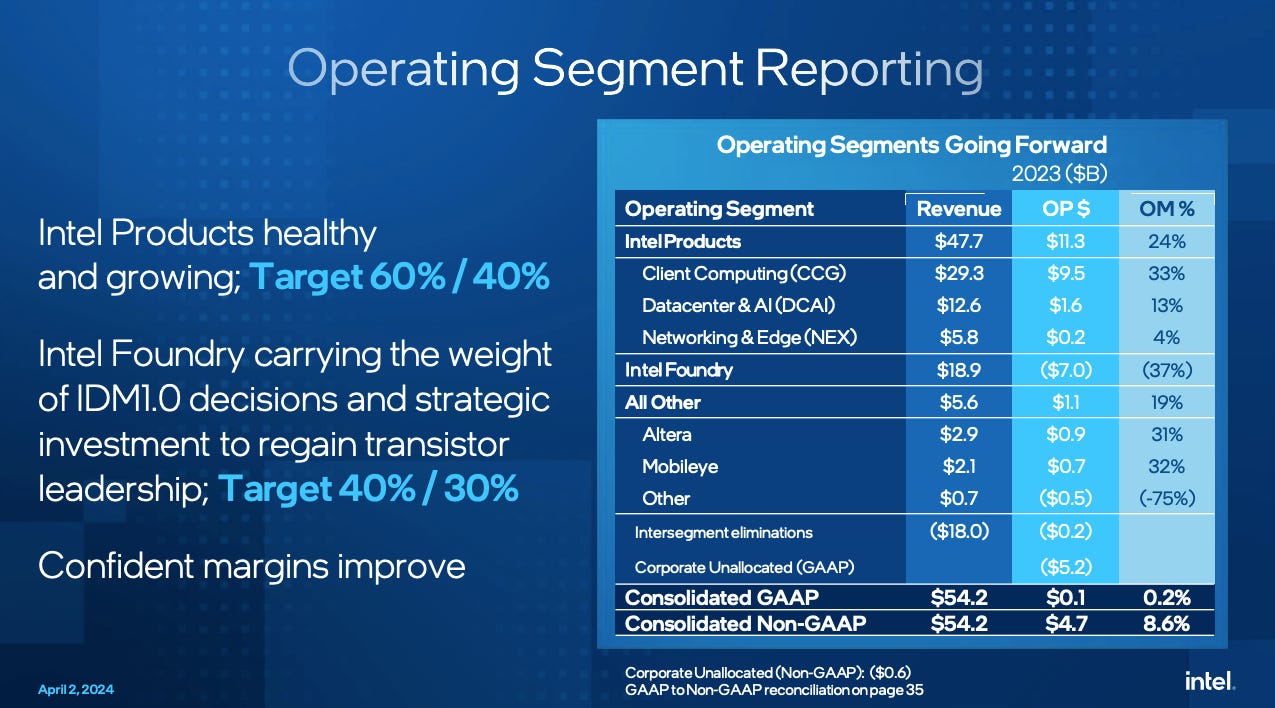

But again, I digress. Going back to the details of the new reporting structure, the slide deck shows how this works in the case of just one year, 2023:

The moniker “Intel Products healthy and growing” in the above graphic seems a tad overly optimistic in our view. While the Client group seems in reasonably decent shape with a 33% operating margin, the same can hardly be said for the Data center group (15% OM) or the Networking & Edge group with an OM of just 4%. Nonetheless, it’s reasonable to assume that the Intel Products P&L can ultimately achieve their targets of 60% gross margin and 40% operating margin.

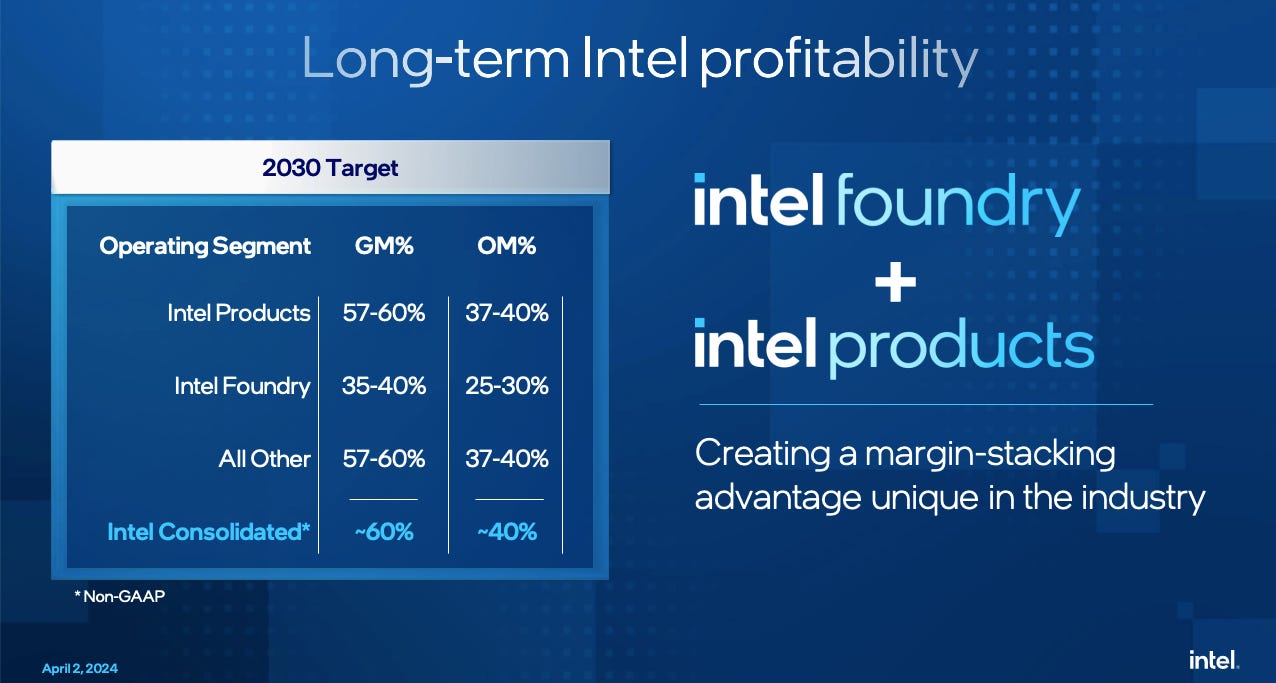

Meanwhile the Foundry P&L presently languishes at negative 37% OM as it “carries the weight of IDM1.0 decisions and strategic investments to regain transistor leadership”. Regardless of how dire the Intel’s Foundry P&L margins are, they are targeted to reach 40% gross margin and 30% operating margin. Timeline for these targets? 2030:

This is where a comparison with TSMC comes in handy. Their Q423 gross margin came in at 53%. So, even by 2030, Intel does not see its foundry P&L gross margin matching TSMC’s? This is in spite of the fact that Intel claims it will retake process leadership with 18A, set to launch in volume in 2026.

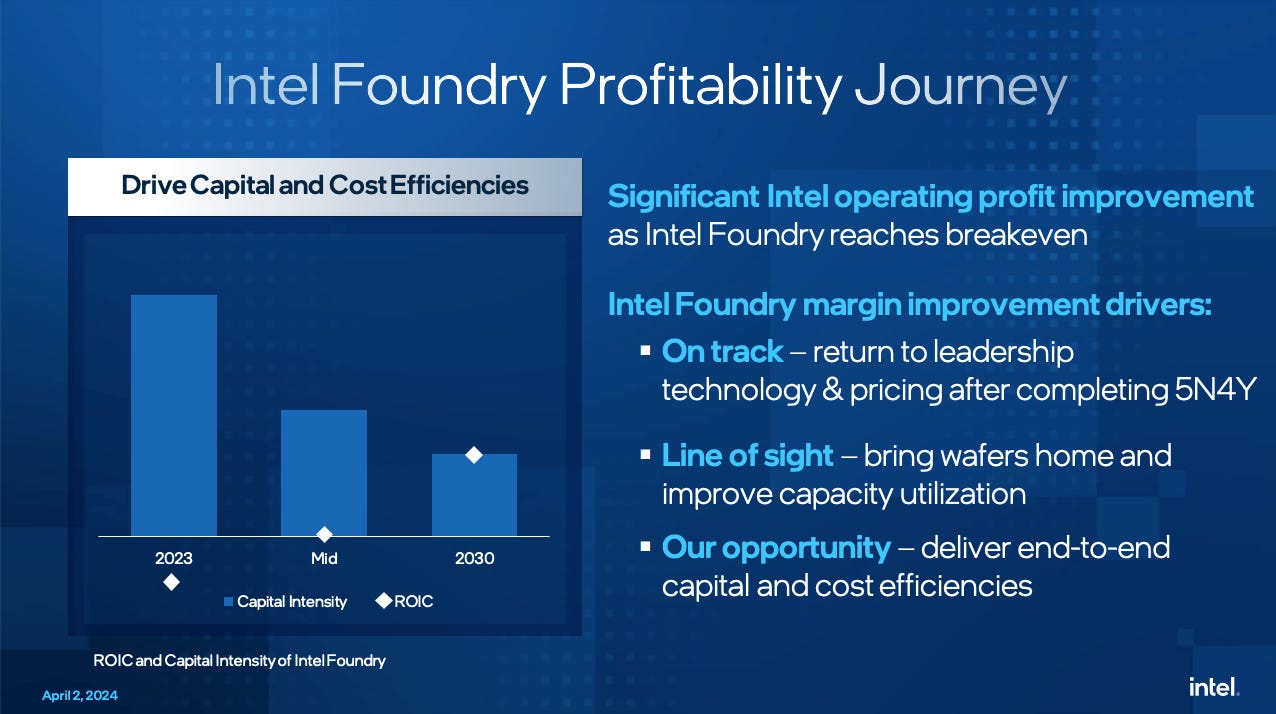

One additional page from the presentation deck is worth highlighting, namely the roadmap for Intel’s Foundry P&L’s ROIC to turn positive:

So, ROIC will stay negative until ~2027 and only hit positive territory somewhere between there and 2030. Yikes!

If we were to summarise what Intel told us on the webinar, it would be along the following lines:

#1 Everything is on track as far as 5N4Y process roadmap is concerned

#2 Intel’s newly defined Foundry P&L has been delivering operating losses of between $5 billion and $7 billion annually over the course of the past three years

#3 Those Foundry P&L operating losses will remain much the same in 2024 and most likely also in 2025

#4 We should frame Intel’s return to profitability, or at least Intel’s Foundry P&L’s return to profitability against the backdrop of when the company’s 18A process hits high volume. This is scheduled to occur 2026.

The bottom line is that Intel bravely presented a framework that clearly tells investors that they better be invested for the long haul, a really long haul. Think 2027. Actually, to be on the safe side, since it got mentioned so much, think 2030. It will come as no great surprise to learn that investors were less than impressed. Intel’s share price has fallen over 10% in the two days since the webinar. Year to date, it’s down ~20%.

Back to the question we posed in the title. Does this new financial reporting structure represent a new era of openness and transparency from Intel or is really just a master class in obfuscation? We’ll strive to answer that question shortly. Perhaps even more importantly, we share some rather telling data points we gleaned from the webinar, mostly during the Q&A session. Specifically, we talk about:

#1 Intel’s projected factory network utilisation through 2030

#2 Intel’s view of their 10nm process (which is still very much in use)

#3 Intel’s mix of process nodes in volume production through 2026 (this will greatly surprise you, and if you are an investor, may alarm you)

#4 Intel told us that they don’t really need wafer volume increase for IFS to reach breakeven. Now, why would that be the case? We explain…

Thanks as always for reading.