KLAC. Looks a Lot Like LRCX!

KLAC. Looks a Lot Like LRCX!

but pay attention to the Q&A discussion on backlog. Very interesting!

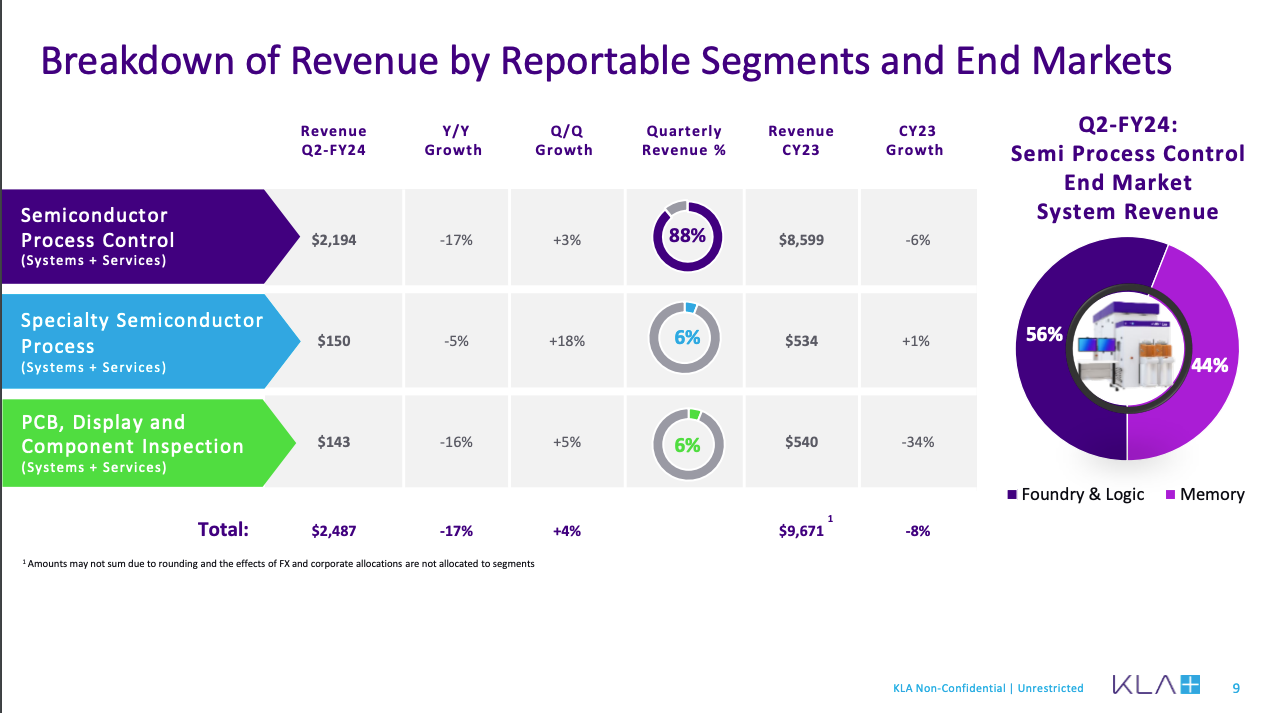

KLAC reported Q423 revenues of $2.49 billion, marginally above the guided midpoint, up 3.6% QoQ but down 15.6% YoY. Net income was $583 million, down $158 million QoQ.

For the calendar year 2023, KLAC recorded revenues of $9.6 billion, down 8% YoY. With the exception of ASML, KLAC outperformed all their other competitors last year, primarily attributable to their relatively smaller exposure to the memory segment.

In what has become a now all-too-familiar pattern, KLAC’s revenue attributable to customers in China remained at an elevated level of 41%, albeit this was a slight reduction from the 43% in the prior quarter.

For what it’s worth, KLAC is confident that their China-related business will remain strong in 2024:

So, for China, CJ, I think overall, for China, it looks pretty flattish year to year. We did benefit from the infrastructure investment that I talked a lot about over the course of the last year or so. I would expect that part of the business to come down some as some of the digestion is happening more so on the wafer side than the reticle side. And so, that obviously will get made up by what I would expect to be slightly higher foundry.

I think the memory piece will shift to potentially ship to another customer. So, I could see that being flattish overall. So, we feel pretty good about the trajectory of China.

In terms of their current year outlook, the similarities with LRCX were striking. Firstly, they also see the WFE market showing a modest increase to the mid-to-high $80 billion range:

For calendar 2024, we currently expect WFE demand to be in the mid to high $8 billion, roughly flat to modestly up from the anticipated level in calendar year 2023.

There was a similar amount of caution and uncertainty in their broader outlook:

We expect that the second half of the calendar year will be stronger than the first half for WFE investment. This WFE estimate reflects our current top-down assessment of industry demand as follows: In memory, we expect WFE investment to be slightly up from low levels with investments focused on high bandwidth memory capacity and leading-edge node development.

As for the memory markets, they warned that utilization will continue to remain at depressed levels until consumer markets reach higher levels of growth:

Both NAND and DRAM fabs are still at low utilization levels as consumer markets have not yet returned to the growth levels needed to bring factory utilization back to the high levels seen in recent years.

Once customers consume this excess capacity and focus on node migration, we would expect to see new investments. Foundry logic is expected to be slightly up with leading edge investment returning to modest growth levels, Legacy investment declining versus 2023, and China legacy node investments remaining relatively flattish to current levels.

All of this translates into a current quarter guidance of $2.3 billion, down 8% QoQ and also down around 5% YoY:

As for guidance, KLA's March quarter guidance is as follows: Revenue is expected to be $2.3 billion, plus or minus $125 million. Foundry Logic is forecasted to be approximately 60%, and memory is expected to be 40% of semi-process control systems revenue.

The company attributed this sequential decline to a delayed customer project:

KLA's overall demand is stabilizing around current business levels, plus or minus the guidance ranges. As of now, this translates into KLA revenue bottoming in the March quarter, driven mostly by a customer project delay occurring in the last couple of months.

This situation should rectify itself in their June quarter where a return to modest sequential growth is expected.

Based on current fast schedules in our June quarter shipment plan, we expect sequential growth to return in the June quarter and continue for the remainder of the calendar year.

Our thoughts on what lies ahead for KLAC in the coming quarters. Spoiler alert, they are very similar to our thoughts on LRCX from yesterdays post :-) Plus we dig a little deeper into the very interesting exchange between analyst Timothy Arcuri and CFO Bren Higgins on the topic of KLAC’s backlog. Definitely food for thought in what transpired between the two!

Thanks as always for reading!

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.