Microsoft Down ~10% Despite Earnings Beat, Raises & CapEx Growth. What Gives?

whatever happened to that token growth metric Microsoft was so proud of last year?

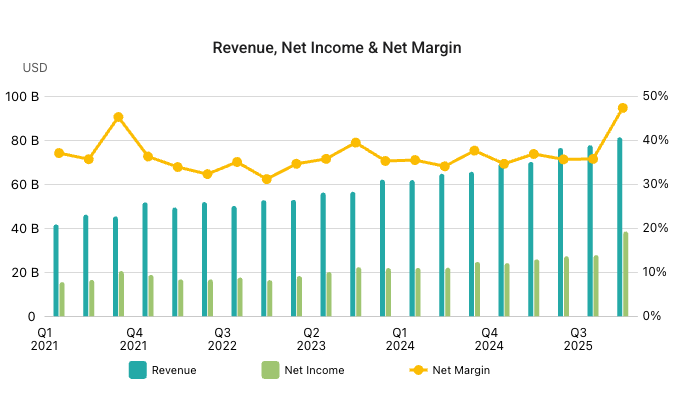

Last week Microsoft delivered a robust Q2FY26 earnings report with revenues of $81.3 billion, up 4.7% QoQ, up 17% YoY and handily beating the $80.6 billion that represented the high end of the guided range

It wasn’t just a beat on revenue, key high level metrics impressed across the board:

Gross margin dollars increased 16% and 14% in constant currency while operating income increased 21% and 19% in constant currency. Earnings per share was $4.14, an increase of 24 and 21% in constant currency, when adjusted for the impact from our investment in OpenAI.

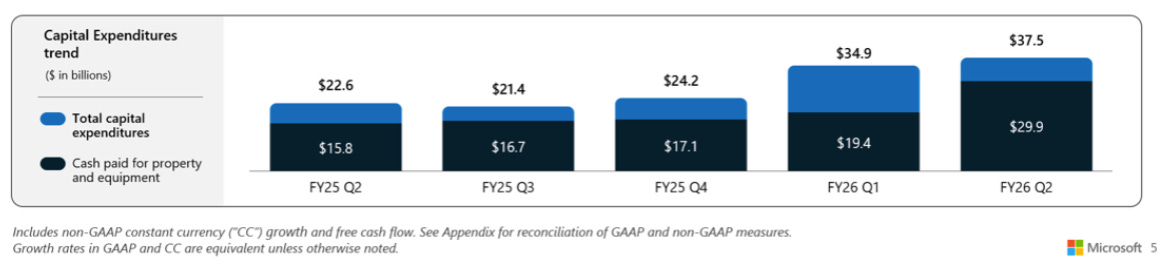

During the quarter, Microsoft spent big time on CapEx, their highest ever quarterly outlay at $37.5 billion. This resulted in the company onboarding 1GW of compute during the quarter:

All up, we added nearly one gigawatt of total capacity this quarter alone.

Despite this unprecedented level of CapEx spending, customer demand continued to exceed supply, a common theme across many of the company’s recent earnings reports

Capital expenditures were $37.5 billion, and this quarter, roughly two thirds of our capex was on short-lived assets, primarily GPUs and CPUs. Our customer demand continues to exceed our supply.

CapEx is expected to decline sequentially in the current quarter

Next, we expect capital expenditures to decrease on a sequential basis due to the normal variability from cloud infrastructure buildouts and the timing of delivery of finance leases.

Unlike last year where Mr. Nadella was clear from the outset that CY25 CapEx would be $80 billion, we haven’t received a specific guide for the current year. However, based on the levels seen in the first two quarters, $120 billion should be around the right ballpark figure, representing a 50% increase YoY.

Looking ahead to the current quarter, Microsoft forecasted as follows:

We expect revenue of $80.65 to $81.75 billion or growth of 15% to %17 with continued strong growth across our commercial businesses, partially offset by our consumer businesses

By all accounts, it was an excellent quarter with solid beats and raises, yet the share price slumped 10% in after hours trading and has remained at that depressed level ever since:

This pricing action sees Microsoft eke out just a 3.7% gain over the past twelve months and down 22.5% from its most recent 52 week high. For a company at the epicentre of the AI boom, and arguably a poster child for same, it’s not a great look.

So what’s going on with Microsoft? Well, the post earnings Q&A session gives a few clues and would point us primarily in the direction of CapEx concerns. Another factor might be their continued (and growing?) reliance on OpenAI, which now comprises 45% of their RPO book:

Approximately 45% of our commercial RPO balance is from OpenAI

There’s also an element of concern regarding weakness in their consumer business.

We expect revenue of $80.65 to $81.75 billion or growth of 15% to %17 with continued strong growth across our commercial businesses, partially offset by our consumer businesses.

Yet none of these factors are entirely new. Yes, the RPO reliance on OpenAI increased, but it was pretty high to begin with. As far as increasing CapEx is concerned, they’ve been telling us quarter after quarter that their data centre build outs are simply not keeping up with demand, and therefore it seems only logical that they need to spend more to capture that opportunity before somebody else does.

What may be weighing heaviest on Microsoft’s share price is something they've stopped telling us two quarters ago, namely Token growth rates. Let’s dig in…