Salesforce @ BOFA Global Tech Conference 2026. Executive Summary & Full Transcript

Event: BofA Securities 2026 Global Technology Conference, Salesforce fireside chat

Format: Bank of America software analyst (host Tal Liani, skeptical, recently initiated coverage on Salesforce) in conversation with Miguel Milano, Salesforce’s President and Chief Revenue Officer (guest)

Date: June 2, 2026

This is probably one of the most consequential fireside chats thus far from the BofA conference. From the get-go, it grabs your attention because the host, Tal Liani, sets up the conversation in an adversarial manner. He has at $160 price target and an underperform rating on Salesforce, which was announced on May 18 last, details here.

Bank of America (NYSE:BAC) just made one of the more contrarian calls on Wall Street regarding the enterprise software giant. Analyst Tal Liani reinstated coverage of Salesforce (NYSE:CRM) with an Underperform rating and a $160 price target, a notable bear take on a stock that still carries a consensus average price target of $268.05. For long-term holders of Salesforce, the call sharpens a debate that’s been simmering all year: is Agentforce actually translating to durable revenue growth?

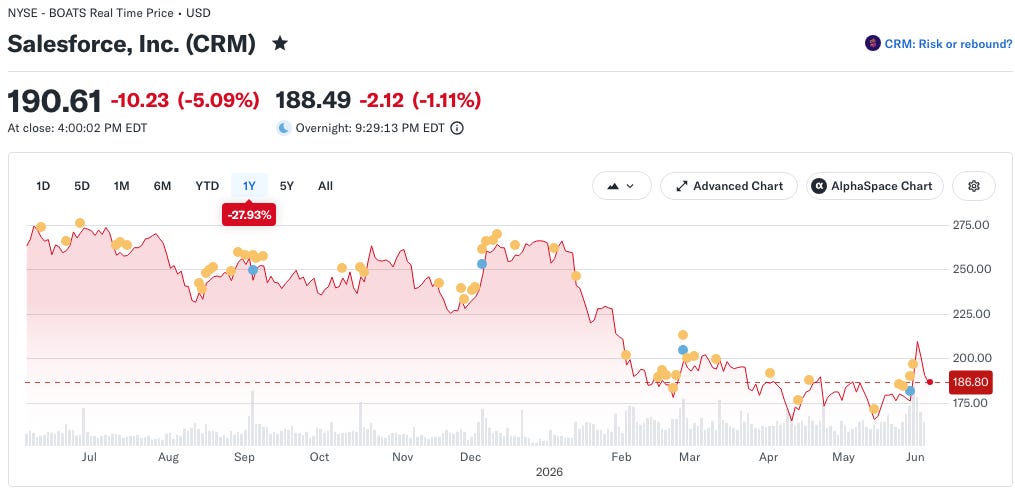

The downgrade lands with Salesforce stock already under pressure. CRM shares last traded near $178.50, down 33% year to date. Liani’s view suggests further downside even after that reset.

Since BofA’s underperform rating, Salesforce has had a brief rally that saw its share price touch $210, but it has since retreated once again and today (June 4) sits at $190

This leaves Salesforce still down 28% over the course of the past twelve months. In any case, after a rather unusual start to chat during which Salesforce’s Miguel Milano heaps praise and admiration on his host, things got off to a very confusing start from my perspective. Here’s verbatim a statement from Milano as he begins to set out his case.

Of course, we bought a company last year that was like a $40-plus billion company. We bought at $1.7 billion, and that helps with the inorganic growth, and we grew 13% revenue, 14% CRPO, we generated $6.7 billion of cash flow. Not bad in one quarter.

Here, one presumes he’s referring to Salesforce’s acquisition of Informatica in May 2025, details here.

Side note: this was a controversial acquisition at the time. Here’s a quick recap, courtesy of Gemini:

The acquisition was a major talking point on Wall Street because it initially collapsed. In early 2024, Salesforce entered advanced talks to buy Informatica when its stock was trading much higher (peaking near $38 per share). Activist investors pushed back, terms couldn’t be agreed upon, and negotiations completely cooled off.

Following the failed 2024 talks, Informatica’s stock plummeted sharply. Salesforce exercised patience, waited for the valuation to reset, and returned to the table a year later to secure the definitive agreement at the vastly reduced $25.00/share ($8 billion) price tag

However, Informatica was not a $40 billion plus company at the time, nor anything close. Furthermore, the purchase price was not $1.7 billion, it was $8 billion

SAN FRANCISCO/REDWOOD CITY, CA — May 27, 2025 — Salesforce (NYSE: CRM), the world’s #1 AI CRM, and Informatica (NYSE: INFA), a leader in enterprise AI-powered cloud data management, have entered into an agreement for Salesforce to acquire Informatica for approximately $8 billion in equity value, net of Salesforce’s current investment in Informatica…

I spent some considerable time trying to figure out what he was actually referring to here and I think Claude may have finally cracked it with this explanation:

Miguel was saying that Salesforce acquired Informatica — a company with a $40+ billion ARR data management business — for approximately $8 billion, but that Salesforce's pre-existing investment stake in Informatica was valued at roughly $1.7 billion, meaning the net new cash outlay was substantially less. The deal closed in late 2025.

Ok fair enough if that’s the answer, but my goodness Milano’s language is so vague and imprecise! Then, to make things worse, Liani interrupts Milano with the following comment:

In the last two weeks, we had a rally. And the rally in software, you are lagging behind. Your stock went up 3%. The others went up 30%. So something in your message doesn’t get across to investors

This is plainly incorrect. Salesforce did rally more than 3%, as Milano quickly pointed out:

But I also need to address some of the inaccuracies. Yes. So the stock went up 8.5% on Friday. It went 9.7% yesterday, Monday. Basically the same as the workday or ServiceNow, et cetera. So I don’t know what you get, the 2%?

Liani then tries to correct himself but only ends up saying something even more confusing and inaccurate

It was since the beginning of the year, so it went down. Okay, sorry. In the last rally.

Anyway, I digress. Milano does go into come considerable detail that will be helpful for investors trying to figure out the direction of travel for Salesforce (and SaaS peers) over the coming quarters. The executive summary that follows is a good start, but there’s a lot more detail in the full transcript attached below the fold.

Executive Summary

The session was framed as a deliberate confrontation: the BofA analyst opened by stating he and Miguel disagreed on his rating, and that the goal was strategy and 10-year positioning, not the quarter. His core challenge: Salesforce’s organic subscription-and-support growth has decelerated to roughly 7.7% from the 20-30% of years past, and the stock has lagged a recent software rally. Where, he asked, is the case that AI reaccelerates the business rather than cannibalizing it?

Miguel’s first move was to dispute the framing. The 7.7% figure, he noted, is organic subscription and support in constant currency; total reported revenue grew 13% and cRPO 14% in the quarter. He also cited roughly $6.7B of operating cash flow as a quarterly figure. He attributed part of the inorganic growth lift to the Informatica acquisition, whose organic revenue he said is now reaccelerating.

The central thesis was that AI is a tailwind, not a headwind, monetized three ways.

First, upgrading existing seats to Agentforce SKUs (”Agentforce 1”) drives an average 60-80% price uplift, and those premium SKUs are now a billion-dollar-plus business growing ~60%.

Second, contrary to the fear that AI shrinks seat counts, seven of the top 10 deals last quarter involved customers adding new human users, i.e. licenses are increasing, not contracting.

Third, and roughly half of agentic monetization, is consumption-based “flex credits” that fuel customer-facing agents and get refilled over time.

On differentiation, Miguel argued Agentforce wins against an estimated ~10,000 competing agentic platforms because it has native access to customers’ codified workflows, CRM context, governance/permissioning built over 27 years, human handoff, and a model-agnostic backend, plus learning from ~29,000 customers.

He conceded prominent industry voices expect the agentic layer to be commoditized, but countered that even commoditized agents will route through Salesforce platforms.

The most forward-leaning topic was the newly launched “Headless 360” strategy: decoupling data, workflow, permission, and agentic layers and exposing them via MCP servers so any external surface (Slack, coding agents, third-party tools) can access Salesforce.

Note: I discussed “Headless 360” in considerable detail some months ago here:

Miguel called it potentially TAM-expanding and “humongous,” explicitly noting it is not yet factored into H2 reacceleration guidance or the FY30 framework (~$63B revenue target, Rule of 50). Monetization is still being negotiated with large customers, since agent-driven access could greatly multiply cost-to-serve for Salesforce.

Other signals: Agentforce grew ~200% year-over-year and ~50% sequentially; an agentic consumption/usage metric the speaker referenced, Agent Workflow Steps (AWS) reportedly doubled quarter-on-quarter and was 7x the year-ago Q1, with Miguel projecting ~500x growth over five years.

Customers remain very early in the adoption cycle, typically 2-4 use cases deployed out of 100-plus mapped across 17 industries, with data readiness the universal first bottleneck (the rationale behind the ~$7.5B Data 360 / Informatica-MuleSoft-Data Cloud layer growing double digits).

Pricing has matured from naive per-conversation metering to ~10 models spanning unlimited-access uplifts, agentic Enterprise License Agreements (ELA), pay-as-you-go, and business-value pricing. Fully-advanced agentic customers reach 3-4x their pre-agentic account value.

Bottom line: Miguel’s pitch is that AI converts Salesforce’s seat-saturation problem into a multi-trillion-dollar digital-labor opportunity, monetized through SKU uplifts, expanding seats, and consumption, with Headless 360 as unguided upside. The analyst remained the skeptic; the rebuttal rested on reacceleration conviction and early but exponential adoption metrics.

Full transcript below the fold. It’s well worth a read if you’re on the SaasPocalypse-is-over-done side of the fence and thinking to jump in.