Semiconductor 2023 Key Indicators In Review, 2024 Forecasts

Semiconductor 2023 Key Indicators In Review, 2024 Forecasts

How will AI-enabled PCs and Smartphones impact unit shipments in 2024?

With the Q423 earnings season finally drawing to a close, it’s time to review our key indicator forecasts for 2023 and present our forecasts for 2024. To begin with, the review. Some of these we have covered in recent posts, so we’ll not spend too much time on them. Semiconductors sales turned out pretty much as we expected with an 8.3% decline versus forecast of a 10% decline.

The WFE segment fared much better than we (or anyone else for that matter) expected, primarily down to a second-half spending spree by Chinese customers. If that unexpected boost had not materialised, I think the forecast for a 20% decline would have been quite accurate.

Silicon wafer area shipments declined by 14.8% versus the forecasted 10%. I think this is a reflection of just how terrible the memory segment was last year, declining 36% versus our forecasted 20%. Foundry (i.e. TSMC) fared marginally better than forecasted with a 8.8% decline versus the expected 10%.

PC shipments fared considerably worse than expected with a 14.8% YoY decline versus the anticipated 10% decline. Smartphone unit shipments surprise on the upside however with a decline of just 3.5% versus the forecasted 10%.

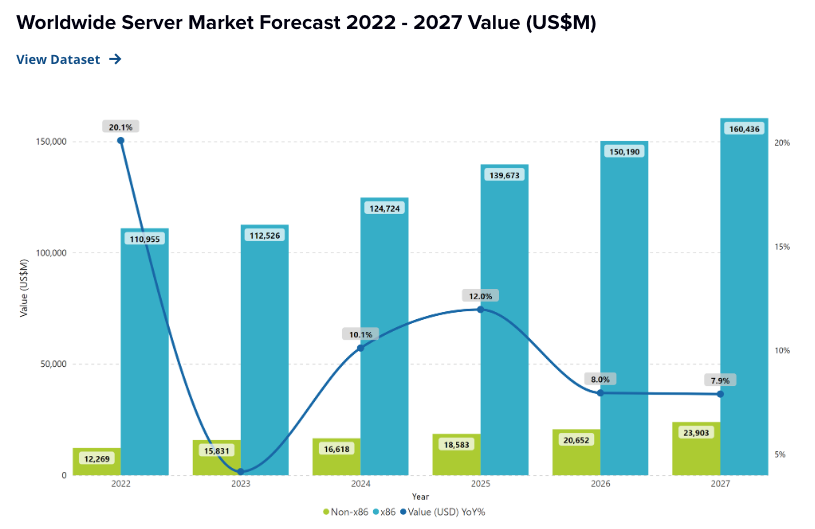

Finally, server unit shipments fared considerably worse than expected with a 20% YoY decline versus our forecasted 10% decline. Note: we’re taking this result from a recent post by OMDIA, details here.

We now expect server shipments of 11.4 million units for the full year of 2023, a decrease of 19% from 2022.

The interesting thing is that, at least according to IDC, server revenues actually grew slightly in 2023, despite the sharp drop in unit shipments:

Despite a huge decline in unit demand (-22.8% year over year), the server market stayed flat in terms of spending growth in the third quarter of 2023 with 0.5% y/y growth, driven by high ASPs, which in turn are mostly related to higher than usual GPU server shipments to hyperscalers.

Note: while the above comment refers specifically to Q323, IDC’s chart for the year as a whole shows that it applies to the full year also:

As for why revenues remained flat while unit shipments declined by >20%, the answer lies in the fact that there was a huge growth in AI-accelerated server shipments where ASPs can be as >20x compared to general purpose servers:

Next up, we present our forecasts for these key indicators for 2024 and share some thoughts on how the year is progressing thus far. Along the way, we dig into the concept of AI-enabled PCs and smartphones and how they may (or may not) disrupt unit shipments in 2024. Thanks as always for reading!

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.