Semiconductor Memory 2023 In Review, 2024 Outlook

Semiconductor Memory 2023 In Review, 2024 Outlook

After reaching a trough in Q123, the Memory segment staged a painfully slow recovery through the second and third quarters of the year. However, Q423 saw a strong upward movement in both memory prices and bit shipments, for both DRAM and NAND.

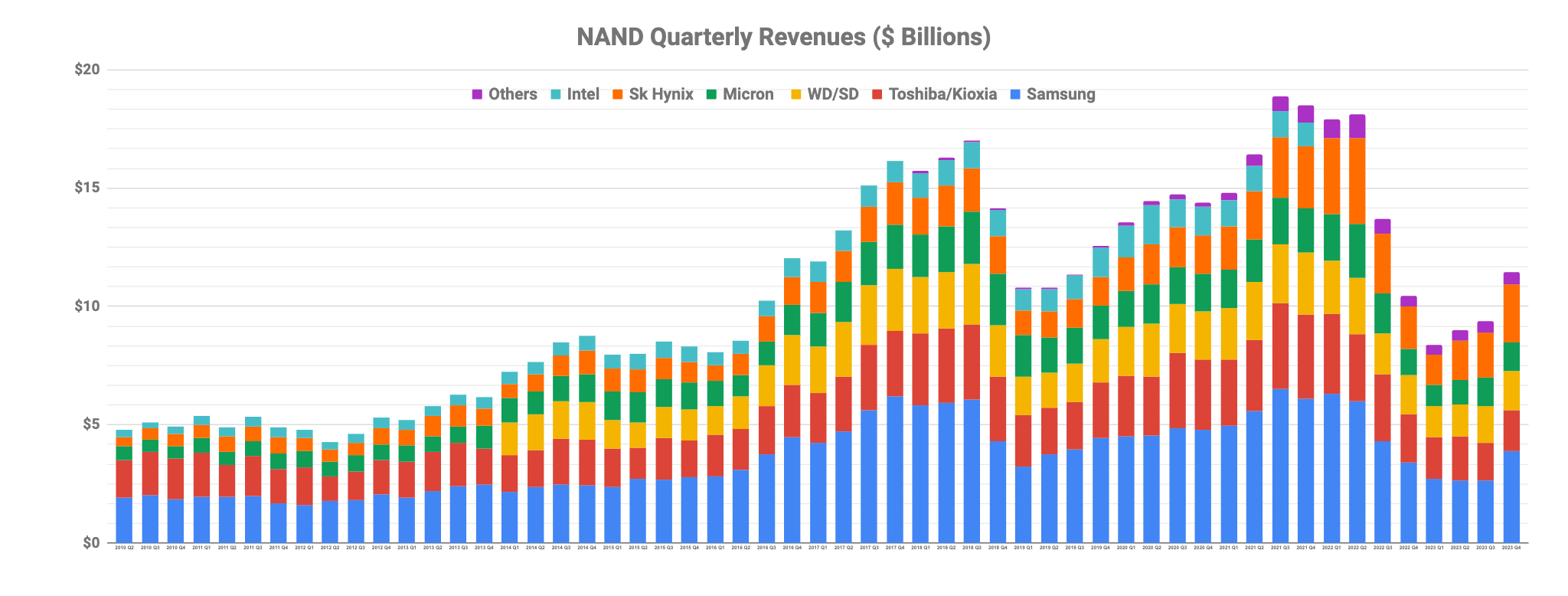

In the case of NAND, Q423 revenues amounted to $11.4 billion, up 22% QoQ and up 9.4% YoY. This was the first YoY increase since Q222!

DRAM staged an even stronger rebound in the fourth quarter with revenues amounting to $17.1 billion, up 30% QoQ and up 39.5% YoY.

Looking at things from an annual perspective, 2023 saw NAND revenues decline by 36.6% to reach $38.2 billion. This followed a decline of 12.2% in 2022.

In the case of DRAM, revenues declined by 17.56% to $66 billion. This followed a 15.6% decline in 2022.

If we combine both DRAM & NAND revenues for 2023, we can see that overall decline was 36% YoY from $140.3 billion to $89.2 billion. This followed a 14% decline YoY in 2022.

Note: our forecast for Memory in 2023 was for a 20% decline. Things obviously turned out far worse than we expected.

There’s no getting away from the fact that 2023 was a brutal year for the memory segment. Actually, as can clearly be seen from the above quarterly charts, things started to go badly wrong in Q322 for both DRAM and NAND. By contrast, Q122 and Q222 were close to all time record highs. This strong performance in H122 distorts the impact of the downturn for the full year 2022, as a result of which full year revenues declined only 14% YoY. Of course, things just got steadily worse through 2023, until the turnaround we witnessed in the fourth quarter.

To underscore just how damaging this latest memory downturn was in terms of the financials of the key players, the following graphic, taken from Micron’s Q4 FY23 earnings report says it all. Revenues in their FY23 were down 49% YoY while net income collapsed from $9.5 billion in FY22 to a loss of $4.8 billion in FY23. Yikes!

Why was the downturn so severe, the worst in over a decade? After all, the previous downturn back in 2019 saw revenues decline 34% YoY, yet all the major players remained profitable in 2019, albeit there may have been a couple of quarters with negative FCF here and there. We discuss this, what was required to exit this downturn and our expectations for 2024 beyond the paywall. Thanks as always for reading!

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.