Sumco Soars But Their Downturn Recovery Still Remains Very Much A Work In Progress

Out of the blue, I got an alert on my screen on last Friday informing me that SUMCO (3436.T) had soared by 18% that day. I was a little taken aback to be honest. I generally follow the silicon wafer segment quite closely. In fact, one of the very first articles I ever wrote about semiconductors concerned silicon wafers:

Over the course of the past two years, the silicon wafer segment has been experiencing a protracted downturn, something I’ve written about many times here.

The problem was that during the broader semiconductor downturn that followed the pandemic boom, customers of silicon wafer companies were obliged to continue ordering and accepting wafers they didn’t need as a result of strict Long Term Agreements (LTAs) they had signed. As a result, inventories soared, and remain mostly at record high levels to this very day.

Back in September 2024, I published the following opinion piece on this topic:

Here are some of the key points I highlighted in that note:

We’re now well into H2’24 and, based on the latest earnings reports, that recovery is starting to happen, albeit slowly. Customer inventory levels are falling, and wafer area shipments are increasing. Yet, valuations for three of the key players, SUMCO, Globalwafers and Siltronic are all back roughly where they were five years ago.

In the case of SUMCO, the situation is even more dramatic in that its share price has fallen by ~45% since mid-July. What’s going on here? As recovery looms, shouldn’t we be seeing greater investor interest, not less? Silicon wafers are the very foundation upon which the current generative AI boom is based and the key players stand to benefit nicely from the growth in AI servers in the coming years

The key silicon wafer players are trading at historic lows. The reasons are clear. Their profitability has been eroded by a combination of falling wafer shipments (down 14% YoY in 2023 and likely down a further 5% in 2024), lower utilisation rates and increasing depreciation costs triggered by huge increases in CapEx over the past two years.

On the bright side, the worst of their downturn is over. We expect to see gradual improvements in revenues and EBIT over the coming quarters. It will likely take 4-6 quarters before they see a return to their most recent highs.

So, here I was basically pointing out that the share prices of the leading silicon wafer manufacturers were mostly at five year lows and that it would take a further 4-6 quarters to work through the inventory levels which would then drive improvements in revenues & EBIT etc.

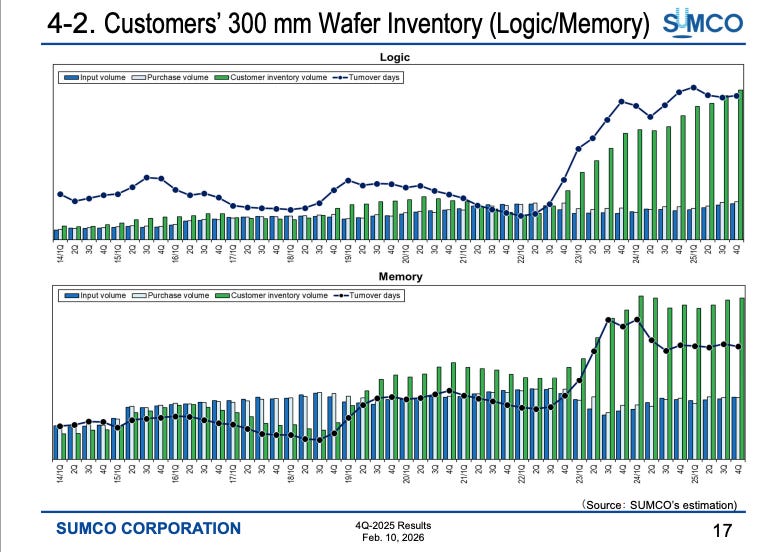

We are now exactly six quarters on from when I wrote that piece, but those improving financials have been painfully slow to materialise. Inventory remains a problem, albeit it’s improving rapidly in certain key segments, e.g. 300mm wafers for high end DRAM,

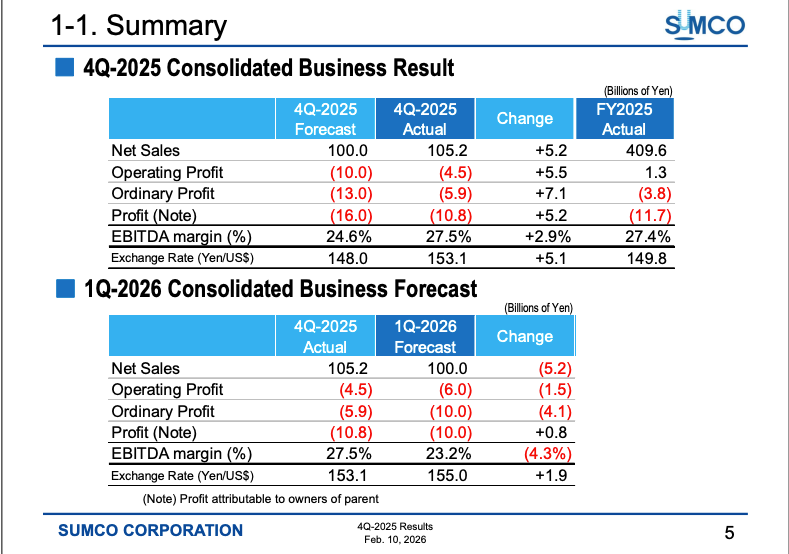

I last checked in on SUMCO during their Q2 2025 earnings call back in February and the news wasn’t looking that great. They guided Q1 2026 down around 5% QoQ

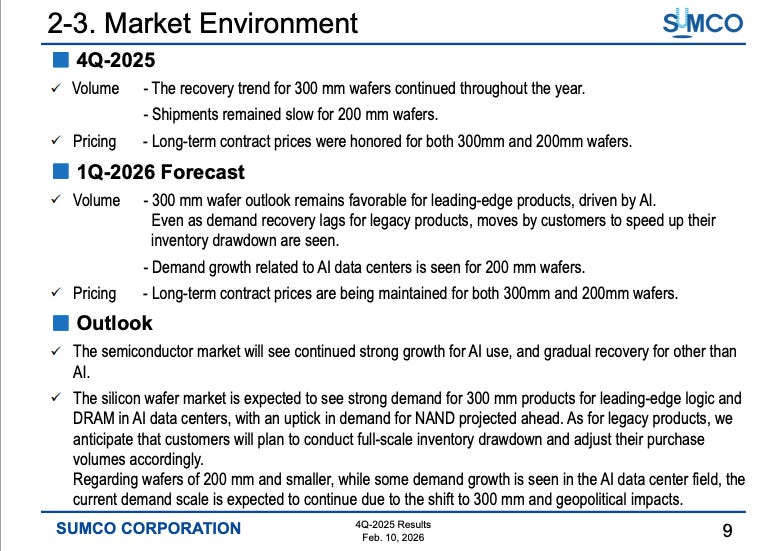

Their usual market outlook slide was a mixed bag at best:

Furthermore, customer. inventory levels have remained stubbornly high, albeit they are levelling off in the case on memory:

So what’s going on with SUMCO and what are we seeing from their peers? Let’s dig in…