SUMCO's Sobering Outlook For Silicon Wafers

SUMCO's Sobering Outlook For Silicon Wafers

However, demand growth driven by AI capable devices is a significant bright spot on the horizon...

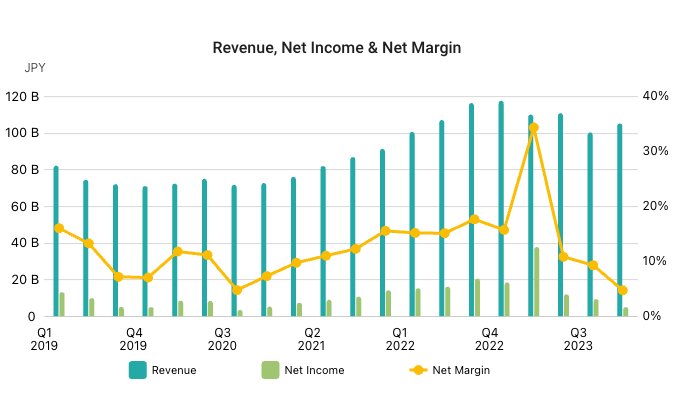

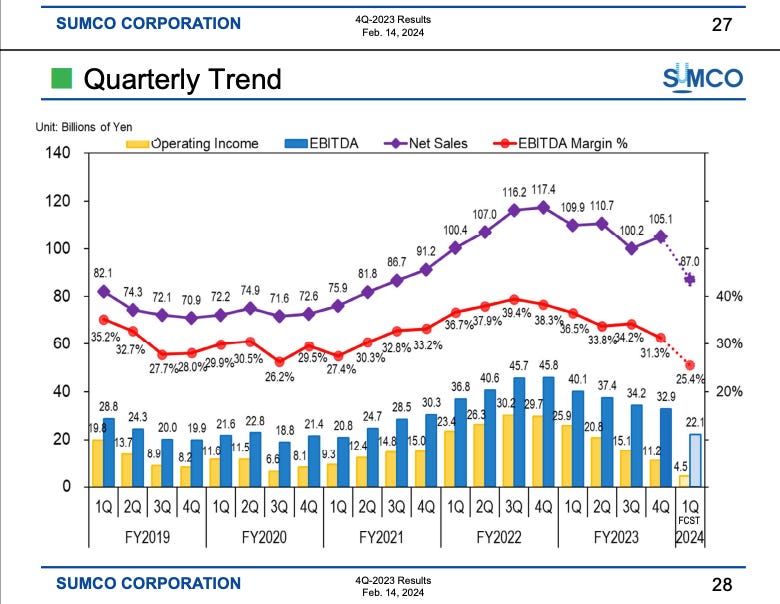

SUMCO last week announced Q423 revenues of ¥105.1 billion, about 5% better than forecasted, up 5% QoQ but down ~10% YoY.

The stronger-than-expected result notwithstanding, EBITDA declined QoQ to ¥32.9 billion. This compares to ¥34.2 billion in the prior quarter and ¥40.1 billion in Q123.

Looking at their quarterly results over the past five years, we can clearly see that all key indicators peaked back in Q422 and have been (mostly) on a gradual downward trend since that time.

Looking ahead to their current quarter guidance, we can see that trend is set to continue with Q124 revenues forecasted to decline 17% QoQ to ¥87 billion. Not surprisingly, EBITDA will also decline 33% QoQ to ¥22.1 billion.

For the full year 2023, SUMCO’s revenues declined by 3.4% YoY to reach ¥425.9 billion. EBITDA declined by 14.7% to ¥144.6 billion.

The primary issue facing SUMCO (and their peers) is that wafer inventories sit at all time historical highs, both for themselves and their customers and for both 200mm and 300mm wafers. We discussed this in detail some months ago here:

Since we wrote that piece, inventory levels have continued to climb across the board, despite SUMCO having initiated production cuts. We review the latest inventory situation, discuss some positive developments when it comes to silicon wafers for AI capable devices and highlight an important change in SUMCO’s medium-to-long term demand forecast, all after the paywall. Thanks as always for reading!

Keep reading with a 7-day free trial

Subscribe to Semicon Alpha to keep reading this post and get 7 days of free access to the full post archives.