Synopsys Crashes On "Major Foundry Challenges". Intel, What Have You Done?

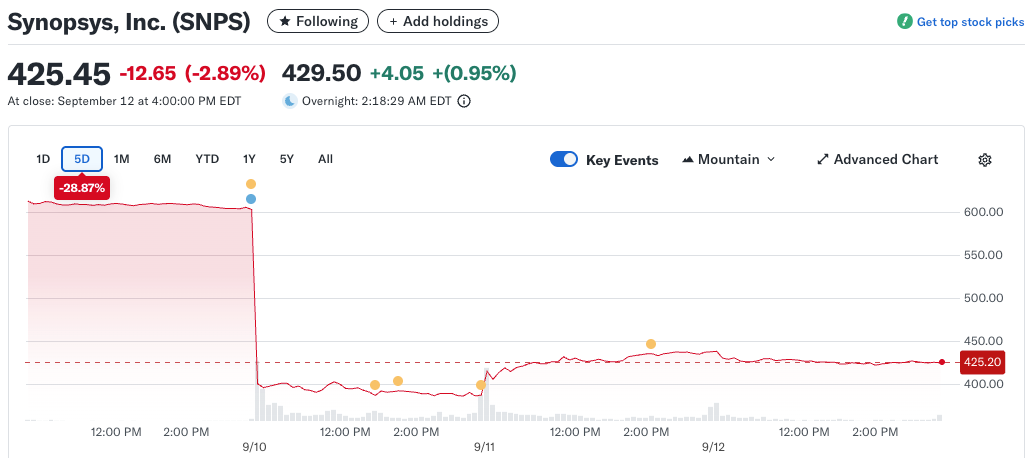

Last week, Synopsys reported Q325 results and guidance both well below expectations causing the share price to collapse over 34% in the immediate aftermath.

Revenue amounted to $1.740 billion, up from $1.526 billion in the year ago quarter, but at the very bottom of the guided range. However, it was the resetting of the company’s full year guide that set the cat among the pigeons:

Now to guidance, which has been updated to include Ansys as well as factoring the continuation of headwinds previously discussed. For fiscal year 2025, the full year targets are: revenue of $7.03 to $7.06 billion

The fact that the newly closed Ansys deal gets included in this full year forecast muddies the waters somewhat when it comes to an apples to apples comparison so I got a little help from Gemini to do the analysis:

Initial Expectations (pre-foundry impact): Before accounting for the negative impact from foundry issues, analysts had projected Synopsys's (the acquirer of Ansys) non-GAAP earnings per share (EPS) for the full fiscal year 2025 to be in the range of $15.11 to $15.19.

Non-GAAP EPS: The company lowered its guidance to a range of $12.76 to $12.80.

That’s a pretty significant downward revision, hence the market reaction, but what caused it in the first place? The company gave three reasons:

Our results were primarily impacted by underperformance in the IP business as we had the expectation of deals that did not materialize, driven largely by the following three factors:

#1 new export restrictions disrupted design starts in China, compounding China weakness;

#2 challenges at a major foundry customer are also having a sizeable impact on the year;

#3 finally, we made certain roadmap and resource decisions that did not yield their intended results.

We shall address each of these three factors in turn shortly, but the general consensus was that the second factor had by far the biggest impact and the most likely candidate for “challenges at a major foundry customer” is of course, Intel.

So, something very significant and very abrupt happened in their dealings with Intel during the quarter. What could that be? Furthermore, if Intel took some drastic action with Synopsys, might they have done the same with Cadence? After all, both EDA companies work closely with Intel, and indeed, both were signed up to help develop the IP libraries to support new customers who might be interested in using Intel’s 18A process, or more likely the 18A-P variant. Cadence reported earnings back on July 29, some six weeks ahead of Synopsys. Furthermore, its share price dropped ~10% in sympathy with Synopsys, albeit it recovered much of that ground over the following two days:

So what’s going on between Intel and Synopsys? Let’s dig in….